Investing in mutual funds is a common method of increasing your savings in India, but any investment involves risks. In 2025, when markets are unpredictable due to global issues, inflationary pressures, and interest rate shifts, knowing these risks is more crucial than ever. Mutual funds collect money from numerous investors to purchase stocks, bonds, or other investments, guided by experts. Although they provide diversification and possible profits, market collapses or inappropriate fund decisions can create losses. The best part? Most risks are preventable with savvy strategies like diversifying investments or selecting the right funds.

Here’s the guide to the most common risks in plain language, gleaned from experts and current trends. We’ll tell you what each risk is, why it occurs, and how to deal with it in practical terms. Beginner or experienced investor, you’ll make wiser choices when you know this. No investment is completely risk-free, but knowing is power that turns pitfalls into steps to take. Let’s lay it out so you can invest with confidence.

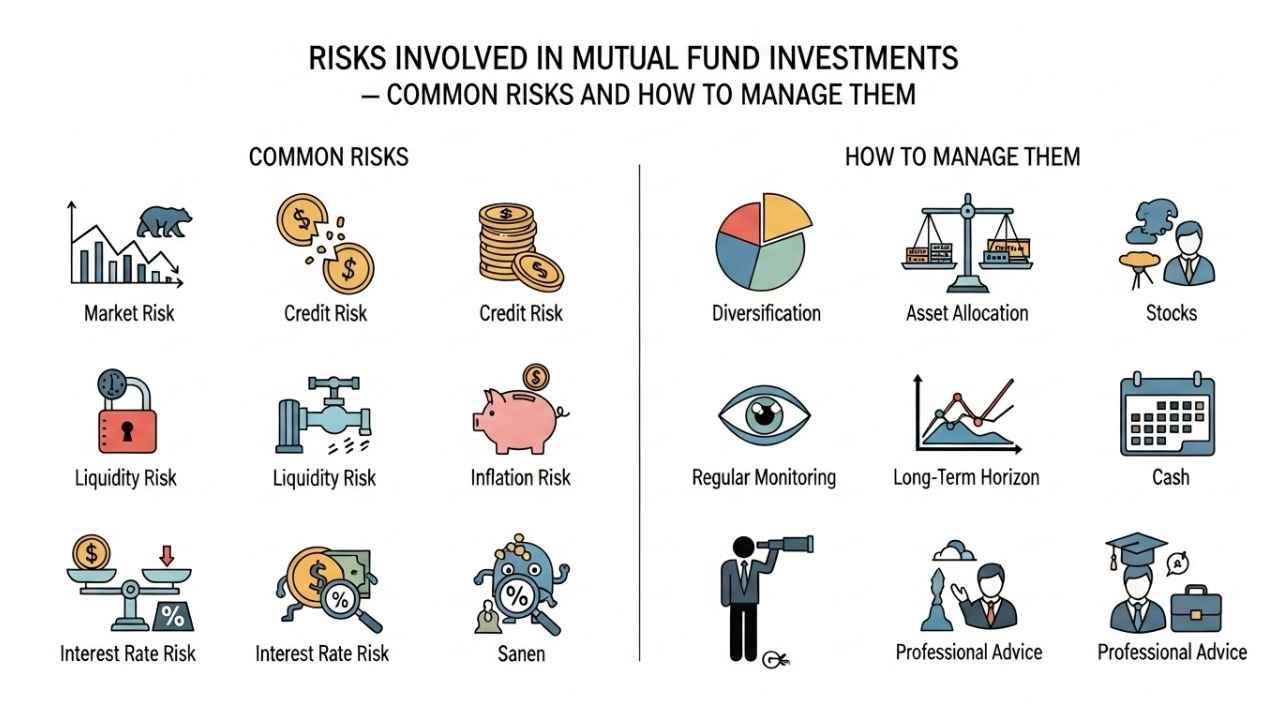

Market Risk: The Ups and Downs of the Stock Market

Market risk, or volatility risk, is one of the largest mutual fund investment concerns. It occurs when your fund’s value decreases because of general market fluctuations, such as economic slowdowns, political upheavals, or global crises. For instance, Indian markets in early 2025 plunged due to concerns of a US recession, impacting equity funds severely. If your mutual fund is invested in shares, a bear market can erase gains in a jiffy. The risk is great in equity funds but less in debt funds. Why should you care? Because it’s difficult to time the market—prices fluctuate wildly, and you can end up losing money if you panic and sell.

Avoiding market risk begins with diversification: Invest your money in various sectors and asset classes, such as combining stocks with debt in hybrid funds. A long-term approach helps too—historical data shows markets recover over 5-10 years, with equity funds averaging 12-15% returns despite dips. Use SIPs (Systematic Investment Plans) to buy units regularly, averaging costs over time. Stay informed via apps like Groww or ET Money, but avoid daily checks to prevent emotional decisions. If you’re risk-averse, opt for large-cap or index funds, which are more stable. In 2025, with SEBI’s new stress tests, funds report volatility more accurately, so you can make informed choices. Check your portfolio periodically—rebalance annually to maintain risk in line. By targeting goals such as retirement over short-term profits, you can weather storms and accumulate wealth over time.

Interest Rate Risk: When Rates Change, Bonds React

Interest rate risk primarily touches debt mutual funds, in which money is invested in bonds or fixed-income instruments. When RBI raises rates to curb inflation—like it did in mid-2025—prices of bonds decline, reducing your fund’s NAV (Net Asset Value). Rate cuts, on the other hand, push prices up. Long-duration funds (bonds that mature in 5+ years) have greater risk because they’re more sensitive to rate changes. For example, an increase of 1% in interest rates can reduce the value of long-term bond fund by 7-8%. It is lower in short-duration funds. Why panic? It can trim returns if you require money in the near future.

To handle it, align fund duration with your investment horizon: Short-time goals? Choose short-duration or liquid funds with less effect. Diversify to dynamic bond funds, where fund managers keep changing holdings depending on rate expectation. Track economic news—RBI statements are crucial. In 2025, with rates firming at 6.5%, experts recommend floater funds that gain from the upward movement of rates. Utilize tools such as duration calculators on Bajaj Finserv or Value Research to measure risk. If rates are likely to dip, lock in for longer durations for gains. Don’t panic; stay invested through cycles as the bond market rebounds. For novices, begin with ultra-short debt funds—low risk, stable 6-7% returns. Meeting with a SEBI-registered consultant can make selections customized. In all, comprehension of interest rates makes this risk a goldmine, making your fixed-income investments secure and profitable.

Credit Risk: The Danger of Defaults

Credit risk happens when issuers of bonds in your debt fund are unable to repay, resulting in defaults. It is most prominent in credit risk funds seeking high yield from lower-rated securities (BBB or below). In India, earlier crises such as the 2018 IL&FS crisis demonstrated how a single default can impact NAVs significantly—20-50% were lost by some funds. Even in 2025, with regulations now tighter, risks still persist if economic slowdown impacts companies. 8-10% returns are guaranteed by high-yield funds but come with this baggage. Equity funds have less, but exposure to corporate adds a layer.

Mitigation starts with adhering to quality funds: Select those backed by AAA-rated bonds for security, even though returns are less (at about 7%). Verify credit ratings through CRISIL or ICRA reports on fund websites. Diversify by issuers—SEBI limits single-issuer exposure to 10%. Select gilt or government bond funds, nearly default-free. Defaults in 2025, after SEBI’s side-pocketing norms, are contained, leaving good assets insulated. Employ ratings such as 4-5 stars from Morningstar for solid recommendations. If you must go into credit funds, cap at 10-20% of portfolio. Track news for issuer health; apps provide alerts. For conservative investors, steer clear entirely—target sovereign debt. By putting quality ahead of yield, you protect capital while generating steadily. Keep in mind, higher returns tend to translate to higher risk, so balance is crucial for peace of mind.

Liquidity Risk: When You Can’t Sell Easily

Liquidity risk means you can’t redeem your fund units quickly without loss, often in illiquid assets like small bonds or stocks. It hit hard in 2020’s Franklin Templeton wind-up, where investors waited months. In 2025, with market growth, it’s rarer but possible in micro-cap or credit funds during stress. Open-ended funds promise daily liquidity, but side-pocketing (separating bad assets) can delay. This risk hurts if you need emergency cash, forcing sales at lower prices.

To manage it, opt for liquid funds or large-cap equity ones with high volumes—easy to offload. Look at AUM (Assets Under Management); larger funds (₹10,000+ crore) are more liquid. SEBI’s mandates in 2025 call for 20% liquid assets in debt funds, minimizing risks. For management, create a safety fund in ultra-short debt (same-day liquidity). Diversify—blend liquid and illiquid for balance. Look at exit loads (charges for pre-withdrawal) and lock-ins. Apps such as Zerodha display liquidity figures. When long-term investing, overlook short-term problems; markets stabilize. Beginners: Begin with ETF or index funds, very liquid. Remain current through AMFI alerts. Through careful plans of withdrawal and the selection of funds that are easily accessible, you ensure cash at the time it is required, converting possible traps into effortless experiences.

Inflation Risk: When Your Returns Don’t Keep Up

Inflation risk reduces your purchasing power when fund returns fall behind inflation. In India, at 2025 inflation of 4-6%, a 7% return fund actually provides 1-3% real gain. Debt funds lose most, with fixed returns not adjusting. Equity can outpace inflation in the long term (12%+ averages) but short-term volatility injects uncertainty. Why so important? Over time, it reduces savings—₹1 lakh today doesn’t buy tomorrow.

Managing it involves beating inflation: Allocate to equity or hybrid funds for higher potential. Gold funds hedge well, as gold rises with prices. Use CPI-linked strategies or dynamic asset allocation funds that shift based on economy. Calculate real returns: Subtract inflation from nominal. In 2025, with RBI targeting 4%, aim for 8-10%+ portfolios. Diversify globally if possible, but NRIs note rules. SIPs help by compounding over time. Review once a year—switch if returns fall below 2-3% real. Instruments such as inflation calculators on BankBazaar estimate needs. For retirees, consider fixed deposits or annuities. Beginners: Prioritize growth funds. By keeping real growth as priority, you safeguard value of wealth, making investments sustain your lifestyle as costs rise.

Concentration Risk: Putting All Eggs in One Basket

Concentration risk is when a fund invests too heavily in limited stocks, sectors, or assets, maximizing loss if they perform poorly. Sector funds (say, pharma) are vulnerable—if healthcare languishes, as in 2025’s post-pandemic realignments, the entire fund loses. Even diversified funds can be concentrated if managers gamble heavily. It’s greater in thematic or small-cap funds but less in broad indices.

To avoid it, diversify your portfolio: Don’t invest more than 20-30% in a single type of fund. Select multi-cap or flexi-cap funds with spread across sizes/sectors. Review top stocks in scheme reports—seek 20+ stocks. SEBI restricts exposure to any one stock to 10%, but keep a watch. Utilize ETFs that track Nifty 500 for coverage breadth. In 2025, with booms in AI and green energy, stay away from over-hype in one theme. Rebalance annually to preserve spread. For new investors, begin with balanced advantage funds auto-adjusting. Tickertape apps display concentration ratios. If risk-tolerant, keep concentrated bets to 10%. By diversifying, you absorb shocks—one rotten apple won’t spoil the basket, inducing growth steady and slow.

Comparison Table: Risks Across Mutual Fund Types

Here’s a simple table comparing common risks in equity, debt, and hybrid funds, based on 2025 trends. It shows risk levels (Low/Medium/High) and key management tips. Data from general insights; actuals vary.

| Risk Type | Equity Funds | Debt Funds | Hybrid Funds | Management Tips |

|---|---|---|---|---|

| Market Risk | High | Low | Medium | Diversify, use SIPs, long-term hold |

| Interest Rate Risk | Low | High | Medium | Match duration to goals, choose floaters |

| Credit Risk | Low | High | Medium | Stick to AAA ratings, limit exposure |

| Liquidity Risk | Medium | Medium | Low | Pick large AUM funds, avoid illiquid assets |

| Inflation Risk | Low (long-term) | High | Medium | Add equity/gold, aim for real returns >4% |

| Concentration Risk | High (if thematic) | Low | Medium | Spread across sectors, check holdings |

Equity faces market swings but beats inflation; debt is safer but rate-sensitive. Hybrids balance both for most investors.

Conclusion

Risks such as market fluctuations or credit default by mutual funds may appear intimidating, but with information and techniques, they can be controlled. In 2025, diversification, long-term investment, and instruments such as SIPs are your best protectors. Recall that greater returns may go hand in hand with greater risks—match decisions to your tolerance and objectives. SEBI regulations provide protection, but individual due diligence is the master key. Begin small, learn by doing, and seek the advice of experts if necessary. Investing prudently not only accumulates money but also forges financial security. Don’t let risks stop you; let them guide smarter decisions for a brighter future.

Learn More:

- How to Start Investing in Mutual Funds in India – Step-by-Step Process for Beginners

- Difference Between Mutual Funds and Stocks – Which is Better for Beginners?

- Understanding NAV (Net Asset Value) in Mutual Funds – What It Means and Why It Matters

thank