Imagine the scenario. You’ve done your research, chosen a mutual fund that suits your investment objectives, and invested your hard-earned cash. Life is going smoothly, and you’re enjoying the benefits of mutual fund investment.

But one fine day, you receive a notice stating that the mutual fund scheme you’ve invested in is being merged with another mutual fund scheme.

Your immediate reaction would be, “What does it mean for my investment? Should I stay, or should I go? Will I lose my hard-earned investment?”

Don’t worry; you’re not alone in the world of mutual fund investment. A mutual fund merger is more common than you think, especially after SEBI introduced new categorization for mutual funds in 2017.

Although the term ‘merger’ sounds complicated, it’s actually quite simple when you understand the concept of mutual fund mergers and what you should do in such a situation. In the coming sections, we will try to simplify the concept of mutual fund mergers for you and also tell you what you should do in such a situation.

What Is a Mutual Fund?

Before we start talking about mergers, let’s just make sure we’re all on the same page when it comes to what a mutual fund is.

“A mutual fund is a professionally managed investment vehicle. That means when you invest in a mutual fund, your money combines with money invested by thousands of other people. A professional manager uses all of this money to invest in a variety of different securities – stocks, bonds, money market instruments, and so forth.”

The best part about a mutual fund? It’s great for people who want to invest in the stock market or bond market but don’t have the time, knowledge, or interest in choosing their own stocks and bonds. The professional manager will do all of this for you.

Easy peasy, right? Time for us to start talking about what happens when all of this money combines.

What Is a Mutual Fund Merger?

A mutual fund merger happens when two or more mutual fund schemes are combined together. The result can go one of two ways:

- The schemes are merged into an already existing mutual fund scheme (one scheme absorbs the other).

- The schemes are combined to create a brand-new scheme altogether.

In either case, the investors in the merging schemes are given units in the surviving or new scheme. Your investment doesn’t just vanish — it gets transferred.

Think of it like two rivers merging into one. The water (your money) doesn’t disappear. It just flows into a different, combined stream.

Why Do Mutual Fund Mergers Happen?

This is an important question. Understanding why a merger is happening can help you decide what to do about it.

The Big Reason: SEBI’s Categorization Rules

In October 2017, SEBI (the Securities and Exchange Board of India) introduced new and broader categories for mutual funds. The goal was to bring consistency and clarity among similar schemes offered by different fund houses.

Before this, it was common for a single AMC (Asset Management Company) to have multiple schemes that were practically the same — similar investment strategies, similar portfolios, similar objectives. This created unnecessary clutter and confusion for investors.

SEBI’s new rules essentially said: No more overlapping schemes. Each AMC was required to have only one scheme per category.

As a result, numerous AMCs had to either consolidate their existing schemes or merge them with other schemes to comply with the guidelines. This triggered a wave of mutual fund mergers across the industry.

Other Reasons for Mutual Fund Mergers

Beyond SEBI’s regulations, there are several other reasons why a mutual fund merger might happen. Let’s look at each one — and more importantly, what each reason means for you as an investor.

1. Rationalization of Costs

Sometimes, fund houses merge schemes to cut operational costs. Running multiple similar schemes is expensive, and merging them can create efficiencies.

What should you do? If your fund has been performing well and the merger seems to be driven purely by the fund house’s desire to cut costs — potentially at the expense of investors — you should seriously consider rejecting the merger and exiting. A fund house that forces changes just to save money, without considering investor interests, may not be the right home for your investment.

2. Holding Onto Assets

In some cases, a fund house might push for a merger to retain its total assets under management (AUM). Rather than letting investors leave a poorly performing scheme, they merge it into a bigger, better-performing one to keep the money within the fund house.

What should you do? Exercise caution. Use your discretion. If asset preservation seems to be the primary motive rather than genuine benefit for investors, take a closer look before deciding to stay.

3. Redemption Anxiety

Sometimes, even a well-performing fund faces a wave of redemptions because conservative investors get spooked — maybe due to short-term market volatility or negative news cycles. To stop the bleeding, the fund house might decide to merge the scheme.

What should you do? If the fund was performing well and the merger is happening mainly because of panicky investors, you can consider continuing to hold your investment. The fundamentals of the fund might still be strong.

4. Merging of Opposites

Occasionally, two schemes with very different investment styles or focus areas are merged together. For example, a sector-specific fund might be merged into a diversified fund, completely changing the nature of the investment.

What should you do? If you had invested in the fund because of its specific sector or theme focus, and the merger changes that focus entirely, it might make sense to redeem your investment. You can then transfer your money to another fund that still aligns with your original investment thesis.

5. Insufficient or Inadequate Performance

This is a common trigger. A fund that has been consistently underperforming might be merged into a better-performing scheme within the same fund house.

What should you do? This one requires careful thought.

- If your fund is the underperformer being merged into a better scheme, that could actually be good news. But take the time to learn about the scheme your money is being moved into. You don’t want your money going from one bad choice to another.

- If your fund is the one performing well and it’s being merged with an underperformer because of the AMC’s flagship scheme’s poor performance, you might want to withdraw and invest elsewhere. You shouldn’t have to bear the consequences of someone else’s poor performance.

What Does SEBI Say? Important Regulations You Should Know

SEBI has put in place several rules to protect investors during a mutual fund merger. Knowing your rights is crucial. Here’s what SEBI mandates:

1. 30-Day Notice Period

Investors must be given a 30-day notice period before the merger takes effect. This gives you time to evaluate the situation and make an informed decision.

2. No Exit Load

If you decide to exit the scheme during this notice period, you will not be charged any exit load. This is a big deal because normally, exiting a mutual fund before a certain period means paying a penalty. But in the case of a merger, SEBI waives this fee entirely.

3. Full Disclosure of Relevant Information

SEBI requires the fund house to provide you with comprehensive information so you can make a well-informed decision. This includes:

- The most recent portfolio of the schemes involved in the merger

- Financial performance data of the schemes since their inception, along with comparisons to relevant benchmarks

- Details about the new combined scheme’s key characteristics, including its investment objective, asset allocation strategy, and other important features

- A numerical example explaining how new units will be allocated to you

- The proportion of total non-performing assets and total liquid assets compared to net assets — both for each individual scheme and the consolidated scheme

- The tax consequences of the consolidation for unitholders

- Any additional disclosures that the Trustees or the SEBI Board may require

This is a lot of information, and it’s provided specifically so that you, as an investor, can make a clear-headed decision. Don’t ignore these documents.

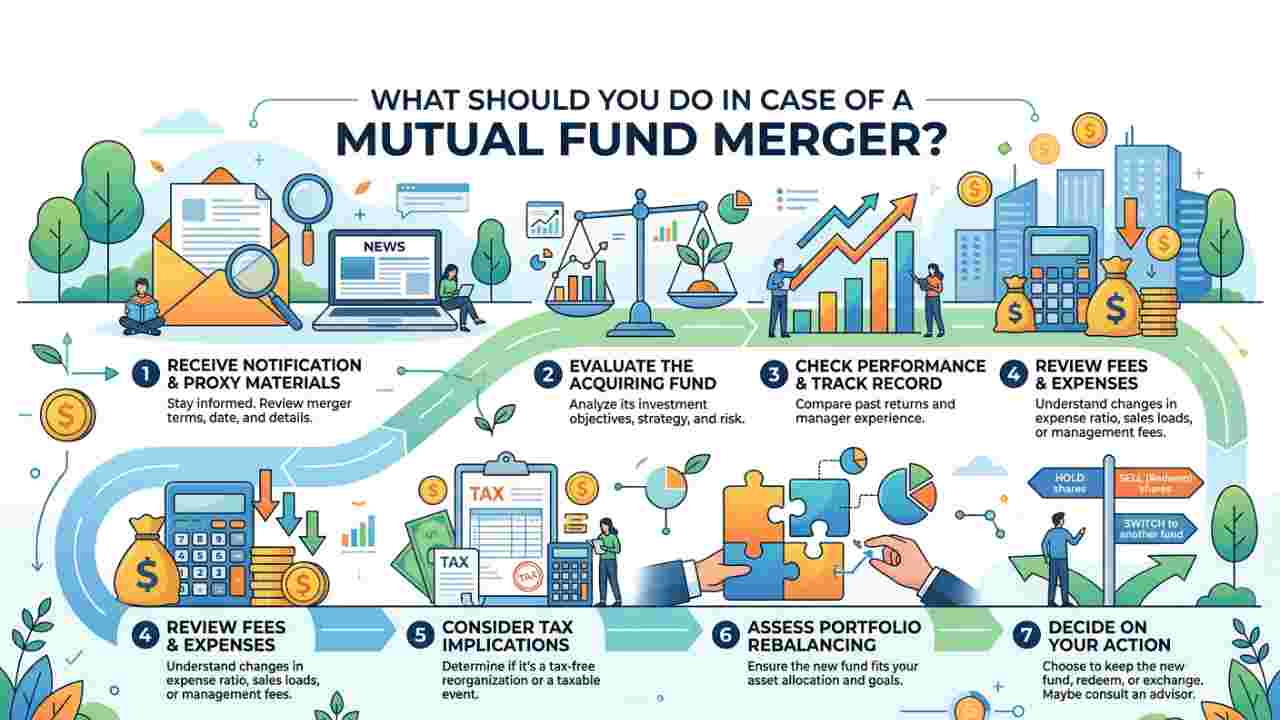

What Should You Do in Case of a Mutual Fund Merger?

Alright, this is the part you’ve been waiting for. Here’s a step-by-step guide on what to do when your mutual fund faces a merger.

1. Thoroughly Read the Unitholder Circular

This is your first and most important step. When a merger is announced, you’ll receive a unitholder circular — a detailed document explaining everything about the merger.

Read it carefully. Don’t just skim through it. Pay close attention to:

- What the new or transferee scheme looks like

- How it aligns (or doesn’t align) with your investment goals

- The impact the merger will have on your existing investment

Understanding the merger’s impact is essential before you take any action. This document is your roadmap.

2. Find Out About the New Portfolio Manager

In some mergers, a new fund manager takes over the combined scheme. This is worth investigating because the fund manager plays a huge role in how your money is managed.

Ask yourself:

- Does the new fund manager’s investment philosophy match yours?

- What is their track record? Have they managed similar funds successfully in the past?

- Do they have a proven investment thesis that makes sense to you?

A great scheme with a poor fund manager can underperform, and vice versa. Don’t overlook this factor.

3. Analyze the Mandate of the New Fund

Every mutual fund scheme has a mandate — its stated investment objective, strategy, and philosophy. When two schemes merge, the resulting scheme’s mandate might be different from what you originally signed up for.

Take a close look at:

- The investment objective of the new or transferee scheme

- Its strategic planning and how it intends to achieve its goals

- Its investment philosophy — is it growth-oriented, value-oriented, income-focused?

- Its past performance (if it’s an existing scheme absorbing your fund)

If the new mandate doesn’t meet your investment needs or doesn’t align with your financial goals, it might be time to exit and find a fund that does.

4. Check for Any Tax Consequences

Taxation is one of those things that can catch you off guard if you’re not paying attention.

During a merger, there are a few tax-related things to keep in mind:

- If you decide to exit the scheme during the notice period and there are capital gains at the time of exit, you will be responsible for paying the applicable taxes. The fund house won’t cover this for you.

- If you choose to stay and receive units in the new or transferee scheme, your holding period does not reset. This is great news. It means the original date you purchased your units will continue to be valid for calculating capital gains whenever you eventually sell. You won’t be treated as a new investor.

Read up on the merger’s methodology and make sure you understand the tax implications clearly. If things feel complicated, consulting a tax advisor is a smart move.

5. Watch Carefully for Any Fee Adjustments

Mergers can sometimes come with changes in the fee structure — the expense ratio, management fees, or other charges associated with the fund.

Here’s an important detail: Any fee changes require a vote from the unitholders before they can be implemented. So you have a say in this.

Pay attention to any proposed fee changes and evaluate whether the new cost structure still makes the fund a worthwhile investment. A fund that suddenly becomes more expensive might eat into your returns over time.

Make sure the fund continues to provide good value for money with a lucrative and fair cost structure.

Quick Summary: Your Action Plan

Let’s put it all together in a simple checklist:

- Read the unitholder circular thoroughly — understand the merger and its impact on your investment

- Research the new fund manager — check their track record and investment style

- Evaluate the new scheme’s mandate — make sure it aligns with your goals

- Understand the tax implications — know what you’ll owe if you exit vs. if you stay

- Review any fee changes — ensure the cost structure is still fair and reasonable

- Make your decision within the 30-day notice period — either stay or exit without paying any exit load

Key Things to Remember

Before we wrap up, here are a few important points worth remembering:

- A mutual fund merger is not the end of the world. Your money doesn’t disappear. It gets transferred to the new or surviving scheme.

- You have 30 days to evaluate the situation and decide what to do. Use this time wisely.

- There is no exit load during the notice period. You can leave without any penalty.

- If you exit and there are capital gains, you will need to pay taxes on those gains.

- If you stay, your original holding period is preserved. The date you first bought your units will still count when calculating capital gains on future sales.

- The concept of a mutual fund merger is not particularly complex, but it does require you to proceed with caution. Don’t just ignore the notice and assume everything will be fine. Take the time to evaluate whether the new arrangement works for you.

Final Thoughts

It might seem daunting at first, but once you get the hang of it, it’s pretty easy. All it takes is being well-informed, reading all the documents carefully, and making an informed decision that suits your financial goals.

You see, SEBI has put in some pretty good regulations to ensure that your interests are being protected. You get to make an informed decision, take 30 days to make it, and exit without having to pay any extra charges. And that’s exactly what these regulations are for.

At the end of it all, it’s your investment decisions that should be made with your goals, your risk tolerance, and your understanding of where your money is being invested. A mutual fund merger is just an opportunity to take a step back, reassess, and make sure that your investments are still aligned with your goals.

If it is aligned with your goals, great! Stay invested. If it’s not, no problem! Take your money out and invest it elsewhere.

Either way, you’re in control. And that’s the most important thing.

Learn More:

- How to Transfer Home Loan from One Bank to Another?

- How to Pay Electricity Bill through Credit Card

- How to Increase Credit Card Limit

- Home Loan Benefits for Women in India

- Best Banks for Gold Loan in India 2025

- Get SBI Yono Personal Loans? Helpful Tips to Get the Loan Fast

- 7-step checklist for fast ICICI Bank personal loan approval

- Airtel Payment Bank Loan: How to Get a ₹5,000 Loan in Just Minutes

Disclaimer: This blog is solely for educational purposes. The securities/investments quoted here are not recommendatory.