If you’re new to mutual funds, you’ve probably come across the term “NAV” and wondered what it actually means. Don’t worry – you’re not alone. Understanding NAV is crucial for making smart investment decisions, and we’ll explain everything in simple terms that anyone can understand.

What is NAV?

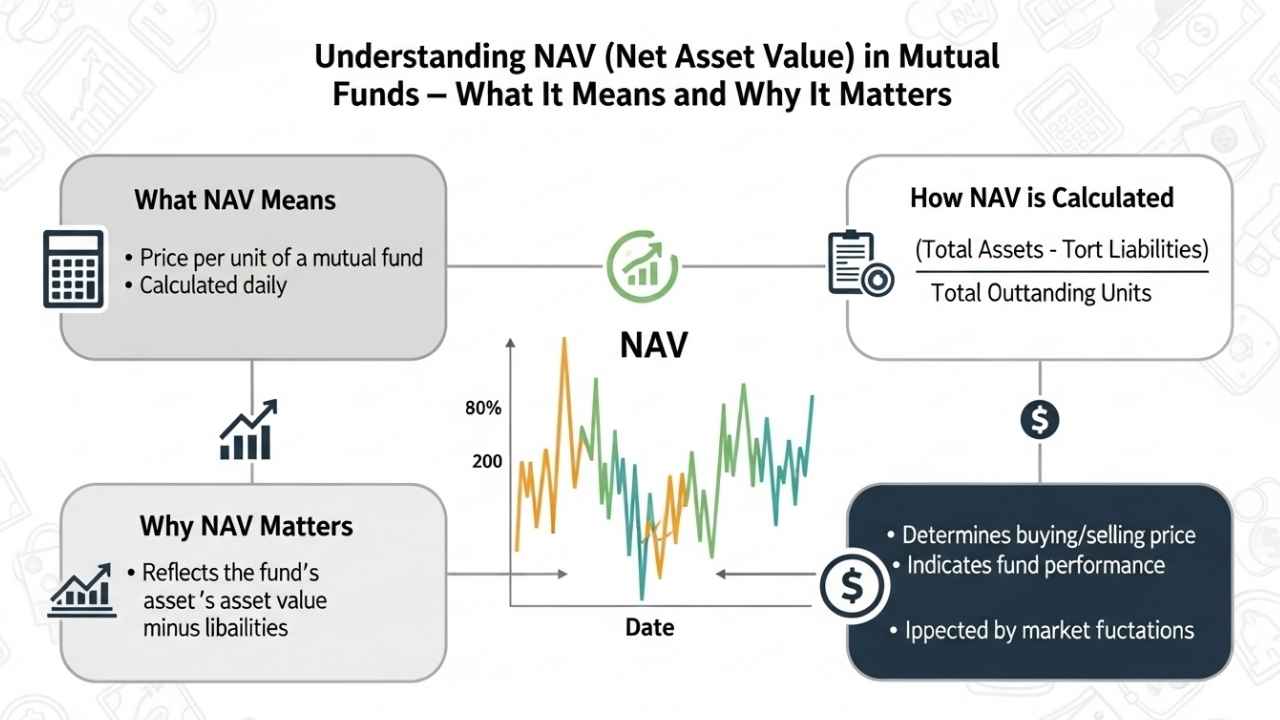

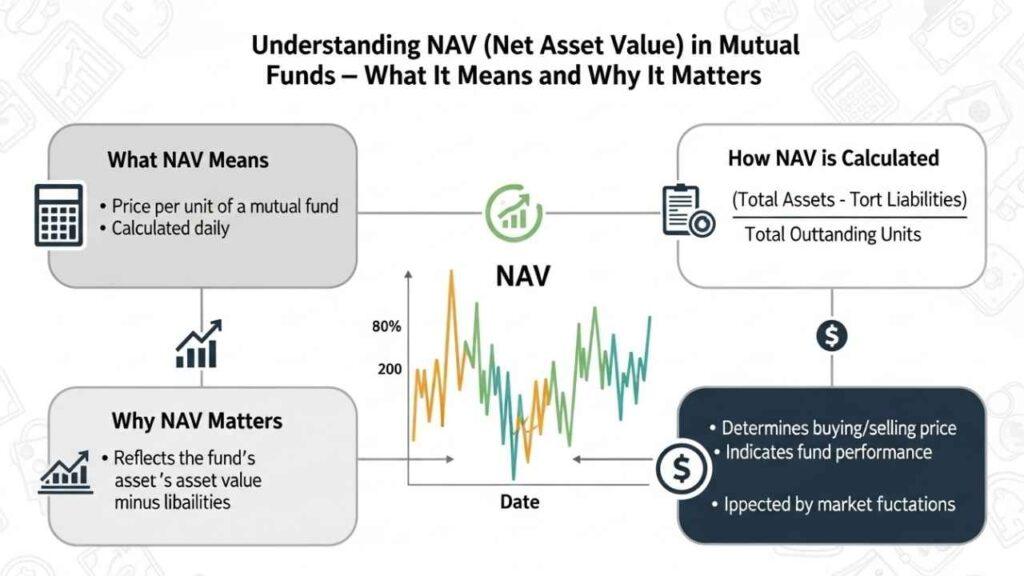

NAV stands for Net Asset Value. Think of it as the price tag of one unit of a mutual fund. Just like a stock has a share price, a mutual fund has a NAV that tells you how much one unit costs.

Here’s a simple way to understand it: Imagine a mutual fund as a big basket containing different stocks, bonds, and cash. The NAV tells you what your share of that entire basket is worth on any given day.

Unlike individual stocks that trade throughout the day, mutual funds only calculate their value once per day after the market closes. This daily calculation gives you the NAV, which becomes the price for all buying and selling transactions.

Key Point: NAV is not just a random number – it represents the real value of all investments held by the mutual fund, divided by the total number of units.

How NAV is Calculated

The NAV calculation follows a straightforward formula that fund houses use every business day:

The NAV Formula

NAV = (Total Assets – Total Liabilities) ÷ Total Number of Outstanding Units

Let’s break down each component:

Total Assets Include:

- Market value of all stocks and bonds held by the fund

- Cash and cash equivalents in the fund’s account

- Accrued interest and dividends (money earned but not yet received)

- Any receivables (money to be received from recent sales)

Total Liabilities Include:

- Management fees and administrative costs

- Outstanding payments to brokers and other service providers

- Accrued expenses (costs incurred but not yet paid)

Outstanding Units:

- The total number of fund units held by all investors

Important: All security values are based on closing market prices from that trading day, ensuring the NAV reflects current market conditions.

Real-World Example of NAV Calculation

Let’s understand NAV calculation with a practical example:

Example: ABC Equity Fund

Fund’s Assets:

- Market value of stocks: ₹100 crore

- Cash in bank: ₹7 crore

- Accrued dividends: ₹75 lakh

- Total Assets: ₹107.75 crore

Fund’s Liabilities:

- Management fees due: ₹1 crore

- Other expenses: ₹25 lakh

- Total Liabilities: ₹1.25 crore

Outstanding Units: 5 crore units

NAV Calculation:

NAV = (₹107.75 crore – ₹1.25 crore) ÷ 5 crore units

NAV = ₹106.5 crore ÷ 5 crore units

NAV = ₹21.30 per unit

This means if you want to buy units of ABC Equity Fund today, you’ll pay ₹21.30 per unit.

How NAV Works in Practice

When You Invest

When you invest ₹10,000 in a mutual fund with NAV of ₹25:

- Units allotted = ₹10,000 ÷ ₹25 = 400 units

When NAV Changes

If the fund’s investments perform well and NAV rises to ₹30:

- Your investment value = 400 units × ₹30 = ₹12,000

- Your profit = ₹12,000 – ₹10,000 = ₹2,000 (20% return)

When You Redeem

If you decide to sell your 400 units when NAV is ₹30:

- Amount you receive = 400 units × ₹30 = ₹12,000 (minus any exit charges)

Key Insight: Your returns depend on the change in NAV, not the absolute NAV value.

NAV vs Stock Price: Key Differences

Many investors confuse NAV with stock prices, but they work very differently:

| Aspect | Stock Price | Mutual Fund NAV |

|---|---|---|

| Frequency | Changes every second during market hours | Calculated once daily after market closes |

| Pricing Basis | Demand and supply in the market | Actual value of underlying assets |

| Trading | Real-time trading possible | Transactions processed at day-end NAV |

| Valuation | May not reflect true company value | Always reflects true fund value |

Important Difference: Stock prices can be influenced by market sentiment and speculation, but NAV always reflects the true underlying value of the fund’s holdings.

When and How NAV is Declared

Daily Declaration Process

SEBI mandates that all mutual funds must declare their NAV daily. Here’s the typical timeline:

- Market closes at 3:30 PM

- Fund houses calculate NAV using closing prices of all securities

- NAV is published on fund websites and AMFI website by evening

- Next day transactions use this published NAV

Where to Find NAV

You can check NAV on:

- Individual fund house websites

- AMFI (Association of Mutual Funds in India) website

- Financial platforms like Groww, Zerodha, ET Money

- Financial newspapers and websites

Pro Tip: NAV is always declared after market hours because it needs the closing prices of all securities in the fund’s portfolio.

Understanding Cut-off Times

Cut-off times determine which day’s NAV applies to your transaction. This is crucial for investors to understand.

Current Cut-off Times (as per SEBI rules):

| Fund Type | Transaction | Cut-off Time |

|---|---|---|

| Equity & Debt Funds | Purchase | 3:00 PM |

| Equity & Debt Funds | Redemption | 3:00 PM |

| Liquid & Overnight Funds | Purchase | 1:30 PM |

| Liquid & Overnight Funds | Redemption | 3:00 PM |

How Cut-off Times Work

Example: You place a purchase order at 2:00 PM on Monday

- You get Monday’s NAV (order placed before 3:00 PM cut-off)

Example: You place a purchase order at 4:00 PM on Monday

- You get Tuesday’s NAV (order placed after 3:00 PM cut-off)

Important SEBI Rule Change

Effective February 1, 2021: NAV allotment is based on when funds are actually received in the mutual fund’s bank account, not when you place the order. This applies regardless of investment amount.

What this means: Even if you place an order before cut-off time, if your payment reaches the fund after cut-off, you get the next day’s NAV.

Common NAV Myths Debunked

Let’s clear up the most common misconceptions about NAV:

Myth 1: Lower NAV Means Cheaper Fund

The Myth: “Fund A has NAV ₹15, Fund B has NAV ₹150. Fund A is cheaper, so I’ll buy more units and make more money.”

The Reality: NAV has no connection to cheapness or expensiveness. What matters is percentage returns, not absolute NAV value.

Example:

- You invest ₹10,000 in Fund A (NAV ₹15) = 667 units

- Your friend invests ₹10,000 in Fund B (NAV ₹150) = 67 units

- If both funds grow by 20%, both of you earn ₹2,000 profit

Myth 2: Higher NAV Means Better Performance

The Myth: “This fund has NAV ₹500, so it must be performing better than the fund with NAV ₹50.”

The Reality: Higher NAV usually means the fund is older, not necessarily better performing. An older fund naturally has higher NAV due to years of growth.

What Actually Matters: Look at percentage returns over time, not absolute NAV values.

Myth 3: NFOs are Better Because of ₹10 NAV

The Myth: “New Fund Offers start at ₹10 NAV, so they’re cheaper than existing funds.”

The Reality: Starting NAV of ₹10 is just an arbitrary starting point. It offers no advantage over investing in existing funds with higher NAVs.

Smart Approach: Evaluate NFOs based on investment strategy, fund manager experience, and portfolio quality, not NAV.

Myth 4: More Units Mean More Returns

The Myth: “I got 1,000 units in one fund vs 100 units in another. The first one will give me higher returns.”

The Reality: Number of units is irrelevant. What matters is the total investment value and percentage growth.

Example:

- 1,000 units × ₹10 NAV = ₹10,000 investment

- 100 units × ₹100 NAV = ₹10,000 investment

- Both investments are identical in value

Why NAV Matters (and Why It Doesn’t)

When NAV Matters:

1. Tracking Performance

NAV helps you monitor your investment’s progress. If NAV increases, your investment value grows proportionally.quantumamc+1

2. Calculating Returns

You can calculate returns using NAV:

Return % = [(Current NAV – Purchase NAV) ÷ Purchase NAV] × 100

3. Understanding Daily Changes

Daily NAV movements show how your fund performed relative to market conditions.

When NAV Doesn’t Matter:

1. Fund Selection

Never choose a fund based on NAV alone. Focus on:

- Fund manager’s track record

- Expense ratio

- Risk-adjusted returns

- Investment philosophy

2. Entry Timing

Don’t wait for NAV to “become cheaper”. Market timing based on NAV is futile since NAV reflects true underlying value.

3. Comparing Different Funds

Comparing NAVs of different funds is meaningless. A ₹500 NAV fund could outperform a ₹15 NAV fund.

Golden Rule: Use NAV to track your own investment’s progress, not to make investment decisions.

Key Takeaways for Investors

Do This:

- Monitor NAV changes to track your investment performance

- Use percentage returns instead of absolute NAV for performance evaluation

- Understand cut-off times to get desired NAV for transactions

- Focus on fund fundamentals like expense ratio, fund manager experience, and portfolio quality

- Check NAV daily on fund websites or AMFI website for accurate information

Don’t Do This:

- Never choose funds based on low NAV

- Don’t assume high NAV means expensive

- Avoid timing investments based on NAV levels

- Don’t compare NAVs across different funds

- Don’t get influenced by NFO marketing about “cheap” ₹10 NAV

Smart Investment Approach:

Step 1: Define your financial goals and risk appetite

Step 2: Research funds based on performance, portfolio, and fund manager

Step 3: Invest based on fundamentals, not NAV

Step 4: Use NAV to monitor progress, not make decisions

Step 5: Stay invested for long-term wealth creation

Learn More:

- Difference Between Mutual Funds and Stocks – Which is Better for Beginners?

- How to Start Investing in Mutual Funds in India – Step-by-Step Process for Beginners

Frequently Asked Questions

Q1: What happens if NAV becomes negative?

Answer: NAV cannot become negative. Even if a fund loses money, the NAV will always be a positive number. However, your investment value can decrease if NAV falls below your purchase price.

Q2: Why does NAV change daily?

Answer: NAV changes daily because the market prices of underlying securities change daily. Since NAV reflects the current value of all holdings, it must be recalculated every business day.

Q3: Can I buy mutual fund units at different NAVs?

Answer: No, all investors who transact on the same day get the same NAV for that day. The cut-off time determines which day’s NAV applies to your transaction.

Q4: Is dividend option NAV different from growth option NAV?

Answer: Yes, dividend option NAV is typically lower than growth option NAV of the same fund. This is because dividend payments reduce the NAV, but this doesn’t mean dividend option is “cheaper” or better.

Q5: How often is NAV calculated?

Answer: NAV is calculated once per business day after market closure. For international funds, calculation may happen after overseas markets close.

Q6: What if I place an order exactly at cut-off time?

Answer: Orders placed exactly at cut-off time may get the same day’s NAV or next day’s NAV depending on when the fund receives your payment. It’s safer to place orders well before cut-off time.

Q7: Does expense ratio affect NAV?

Answer: Yes, expense ratio is deducted daily from the fund’s assets before calculating NAV. Higher expense ratios result in lower NAV growth over time.

Q8: Can NAV predict future fund performance?

Answer: No, NAV cannot predict future performance. Past NAV trends might indicate historical performance, but future returns depend on market conditions and fund management quality.

Remember: NAV is a tool to understand your investment’s current value and track performance. Use it wisely, but never let it drive your investment decisions. Focus on fund quality, your financial goals, and long-term wealth creation.

Disclaimer: This article is for educational purposes only and should not be considered as financial advice. Please consult with a qualified financial advisor before making investment decisions. Mutual fund investments are subject to market risks, read all scheme-related documents carefully.