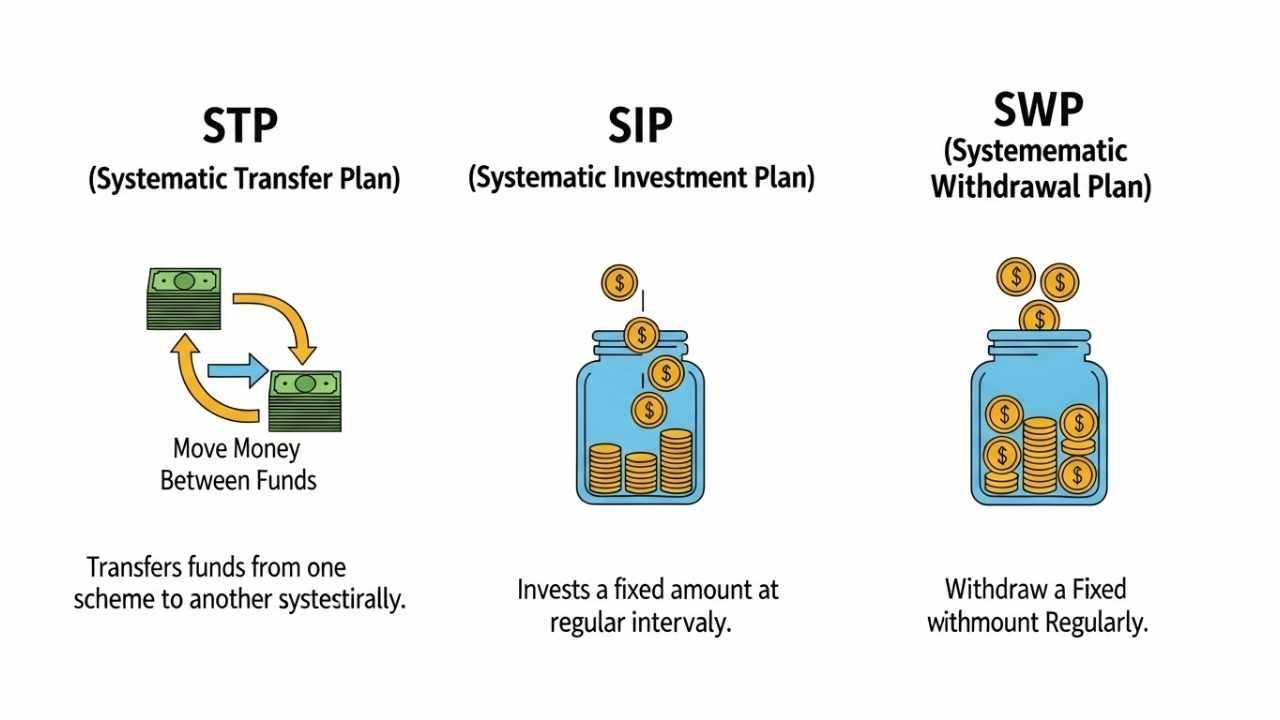

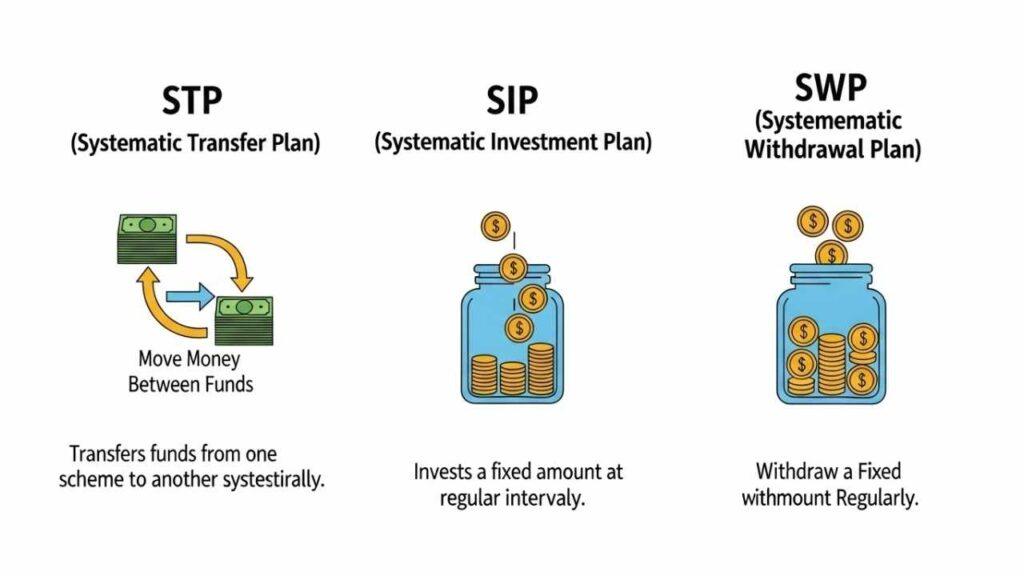

In mutual fund investment, money is invested and withdrawn differently. There are three most used methods: SIP (Systematic Investment Plan), SWP (Systematic Withdrawal Plan), and STP (Systematic Transfer Plan).

It sounds strange, but at first glance, these words may look perplexing. However, they are simple. SIP assists you in investing regularly, SWP assists you in withdrawing regularly, and STP assists you in transferring money systematically between funds.

All three serve different purposes. If you understand the difference between SIP, SWP, and STP, you will be able to choose the correct strategy according to your intention—whether wealth creation, regular income, or risk balancing.

What is SIP (Systematic Investment Plan)?

A Systematic Investment Plan (SIP) is a simple method to begin investing in mutual funds. Rather than investing a large sum at one time, SIP enables you to invest a fixed sum at fixed intervals (weekly, monthly, or quarterly).

For instance, if you spend ₹2,000 per month in a mutual fund, that’s an SIP. With time, that small practice increases your wealth because of compounding. The second major advantage of SIP is rupee cost averaging—you purchase more units when the price is low and less when it’s high, which spreads your cost.

SIP is most suitable for new investors, salaried individuals, and long-term investors who do not need to time the market and wish to accumulate wealth over a period of time.

What is SWP (Systematic Withdrawal Plan)?

A Systematic Withdrawal Plan (SWP) is the reverse of SIP. Rather than investing every month, you withdraw a predetermined amount from your mutual fund investment at periodic intervals.

Assume you have ₹10 lakh in a mutual fund. You can create an SWP to withdraw ₹25,000 per month. The fund redeems each month the necessary units to make you the predetermined amount, and the remaining money remains invested and grows.

SWP is best for retirees or anyone who needs a steady secondary income. It functions as a pension—you receive a steady cash flow without liquidating all your investment at once.

What is STP (Systematic Transfer Plan)?

A Systematic Transfer Plan (STP) enables you to shift money from one mutual fund to another at frequent intervals. Most individuals shift from a debt fund to an equity fund (for appreciation) or from an equity fund to a debt fund (for security).

For instance, suppose you get a bonus of ₹5 lakh. Rather than invest the entire amount in an equity fund all at once (which may prove hazardous), you can keep it in a liquid fund and begin an STP of ₹50,000 every month into the equity fund. In this manner, your money earns returns in the liquid fund and enters the equity market step by step.

STP is perfect for lump sum investors who wish to minimize market timing risk and diversify their portfolio wisely.

Comparison: STP vs. SIP vs. SWP

Here’s a simple table to help you understand the key differences:

| Feature | SIP (Systematic Investment Plan) | SWP (Systematic Withdrawal Plan) | STP (Systematic Transfer Plan) |

|---|---|---|---|

| Purpose | Regular investment | Regular withdrawal | Regular transfer between funds |

| Cash Flow | Outflow (money goes from you to fund) | Inflow (money comes from fund to you) | Both (outflow from one fund, inflow to another) |

| Best For | Beginners, salaried, long-term investors | Retirees, people needing monthly income | Lump sum investors, portfolio balancing |

| Risk | Market risk, but reduced with rupee cost averaging | Market risk if equity fund is source, safer in debt | Market risk depends on target fund |

| Example | Invest ₹2,000/month in equity fund | Withdraw ₹20,000/month from debt fund | Transfer ₹50,000/month from liquid fund to equity fund |

Conclusion

SIP, SWP, and STP are three simple yet powerful strategies in mutual funds.

- SIP is for those who want to build wealth gradually with small, regular investments.

- SWP is for those who want steady income without redeeming all their money at once.

- STP is for those who have a lump sum and want to move it into the market systematically to reduce risk.

Each strategy has a specific purpose. The selection is based on your investment objectives, risk tolerance, and life stage. Most investors find that combining SIP, SWP, and STP works to create an ideal combination of growth, income, and protection.

Learn More:

- How to Start Investing in Mutual Funds in India – Step-by-Step Process for Beginners

- Difference Between Mutual Funds and Stocks – Which is Better for Beginners?

- Understanding NAV (Net Asset Value) in Mutual Funds – What It Means and Why It Matters

- Risks Involved in Mutual Fund Investments – Common Risks and How to Manage Them

FAQs

1. Can I use SIP, SWP, and STP together?

Yes, many investors use a mix of all three to balance growth, income, and safety.

2. Which is better for beginners—SIP or STP?

For beginners with limited savings, SIP is better. STP is suitable if you already have a lump sum.

3. Is SWP safe for retirement income?

Yes, if you choose a balanced or debt fund, SWP can provide steady income during retirement.

4. Do these plans guarantee returns?

No, returns depend on market performance, but spreading investments/withdrawals reduces risks.

5. What is the minimum amount needed for SIP, SWP, or STP?

Most mutual funds allow you to start with as little as ₹500–₹1,000 per month.