Let’s face it. At times, when you start learning about mutual funds, the number of funds available in the market can be quite bewildering.

But let’s put our minds at ease. At the most basic level, mutual funds are of only two types: equity funds and debt funds. So when you understand the basic difference between the two, everything else falls in place.

So if you have been wondering about the basic difference between equity funds and debt funds and which one of the two you should opt for, then you are at the right place.

In this article, we will explain equity funds and debt funds in the simplest way possible. No jargon. No financial words that will confuse you. Just a basic and honest comparison.

Why Mutual Funds in the First Place?

Before we dive into the differences between equity and debt funds, let’s take a quick step back and see why mutual funds are something that should be considered at all.

Mutual funds are one of the most popular ways to invest in the stock market—and for good reason.

Firstly, there’s the aspect of diversification. When you invest in mutual funds, your money isn’t put into just one stock or bond; it’s spread out over many different investments. That means if one stock goes down, your entire investment isn’t going down with it. That’s a major benefit of mutual funds over individual stocks.

Secondly, there’s the potential for greater returns. When compared to something like a savings account or even a fixed deposit, mutual funds have the potential to help your money grow more effectively.

Now, when it comes to mutual funds, two major types of funds stand out: equity funds and debt funds. While they may be different, they’re both unique in their own ways. Let’s take a look at them.

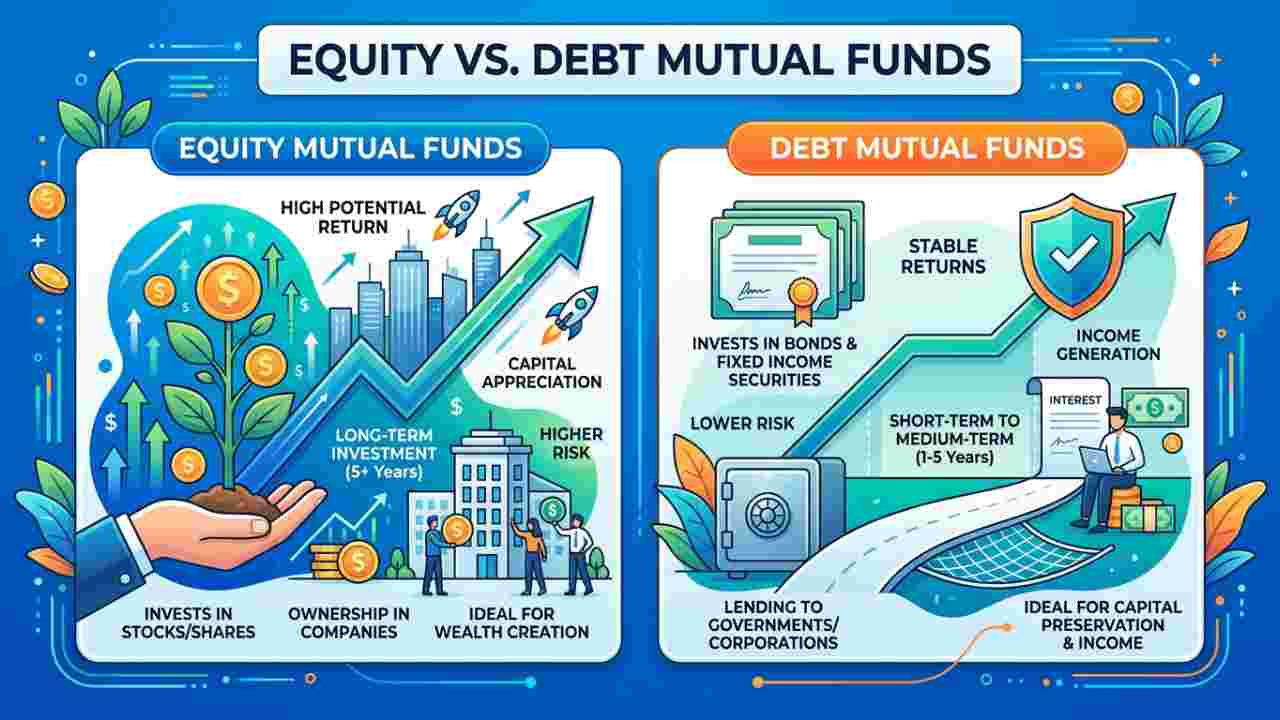

What Are Equity Mutual Funds?

Equity mutual funds are funds that invest primarily in stocks — that is, shares of companies listed on the stock market. When you invest in an equity fund, your money is used to buy ownership stakes in various companies. If those companies do well, the value of your investment goes up. If they don’t, it goes down.

Equity funds are the most common type of mutual fund in India. They’re also known as open-ended equity funds because you can buy or sell your units at any time.

What Makes a Fund an “Equity Fund”?

For a mutual fund to be officially classified as an equity mutual fund, it needs to invest more than 60% of its total assets in equity shares of different companies. The remaining balance can go into money market instruments or debt securities, depending on the scheme’s objectives.

Where Do Equity Funds Invest?

Equity funds invest in shares of both listed and unlisted companies. However, they typically lean toward large, well-established companies with high market capitalization. Market capitalization is simply the total market value of a company — calculated by multiplying the share price by the total number of shares.

The fund manager has the freedom to choose their investment style. They might go with a growth-oriented approach — picking companies expected to grow rapidly. Or they might take a value-oriented approach — picking companies that seem undervalued and have the potential to rise. The goal is always the same: maximize returns for investors.

How Do Returns Work?

The returns on equity funds depend on several factors:

- How the overall stock market performs

- The specific companies the fund has invested in

- Government policies and regulatory changes

- Economic conditions both domestically and globally

Because of these variables, equity funds can be volatile in the short term. Your investment might go up 15% one year and drop 10% the next. That’s the nature of the stock market.

However, over the long term — we’re talking five, ten, fifteen years — equity funds have historically generated better returns than fixed deposits, savings accounts, and debt-based funds. That’s their biggest draw.

Who Are Equity Funds Best For?

Equity funds are best suited for long-term investors who:

- Can stay invested for at least five years or more

- Are comfortable with short-term market fluctuations

- Want their money to grow significantly over time

- Have financial goals that are years away — like retirement, a child’s education, or buying a home

If you’re someone who checks their portfolio every day and panics at every dip, equity funds might test your patience. But if you can ride out the short-term waves, the long-term rewards can be substantial.

Key Factors to Consider Before Investing in Equity Mutual Funds

Excited about equity funds? Hold on — before you invest, make sure you’ve thought about these important factors.

1. Size of the Fund

The size of a mutual fund (also known as Assets Under Management or AUM) tells you how much total money the fund is managing.

Why does this matter? Because fund size can impact performance.

If you’re planning to invest a large amount, a very small fund might not be able to deliver the returns you’re hoping for. On the other hand, an extremely large fund can sometimes become unwieldy — it becomes harder for the fund manager to make quick, nimble investment decisions.

Look for funds with a healthy, well-established corpus. Not too small, not excessively large.

2. Expense Ratio

The expense ratio is one of the most important numbers to look at before investing in any mutual fund. It represents the annual fee you pay for the fund’s management — expressed as a percentage of your total investment.

Here’s the thing about expense ratios: they eat into your returns every single year. A fund with an expense ratio of 2% takes 2% of your investment value as fees annually. Over time, even a small difference in expense ratio can add up to a significant amount of money.

So always compare the expense ratios of similar funds. A lower expense ratio means more of your money stays invested and working for you.

3. Risk-Reward Ratio

The risk-reward ratio helps you understand whether the potential returns of a fund justify the risk you’re taking.

Every investment has some level of risk. But the question is — are you being adequately compensated for that risk?

A fund with a poor risk-reward ratio means you’re taking on a lot of risk but not getting much in return. That’s not a good deal. You want to find funds where the potential upside is worth the downside risk.

This is where research and comparison come in. Look at how the fund has performed historically compared to similar funds and benchmark indices. Has it rewarded investors well for the risk they took? If yes, that’s a positive sign.

What Are Debt Mutual Funds?

Now let’s shift gears and talk about the other major category — debt mutual funds.

Debt funds invest in fixed-income instruments. These include:

- Government securities (bonds issued by the government)

- Corporate bonds (bonds issued by companies)

- Treasury bills

- Debentures

- Commercial papers

- And other money market instruments

Unlike equity funds where you’re buying ownership in companies, with debt funds, you’re essentially lending money to governments or corporations. In return, they pay you interest at regular intervals.

The Core Appeal of Debt Funds

The biggest attraction of debt funds is stability. They offer relatively fixed and predictable returns. There’s no dramatic roller coaster ride like you sometimes experience with equity funds.

Debt funds are considered less risky than equity investments. That makes them a favorite among investors who have a lower risk tolerance — people who value the safety of their money over the possibility of high returns.

However, this safety comes at a cost. The returns from debt funds are generally lower than equity funds. It’s the classic trade-off: less risk means less reward.

Who Should Consider Debt Funds?

Debt funds are ideal for:

- Investors with a low to moderate risk appetite

- People who want stable, regular income from their investments

- Those looking for a better alternative to savings accounts or fixed deposits

- Investors with short to medium-term financial goals

Smart Ways to Use Debt Funds

Debt funds are more versatile than many people realize. Here are two practical ways investors commonly use them:

As a smarter alternative to savings accounts: Let’s face it — the interest rate on a regular savings account is pretty low. Instead of letting your money sit there barely growing, you could invest in liquid funds (a type of debt fund). Liquid funds typically offer returns in the range of 7-9% — significantly better than a savings account. And the best part? You don’t compromise on liquidity. You can access your money when you need it.

As a better option than fixed deposits: Planning to invest for 3-5 years and thinking of a bank FD? Consider a dynamic bond fund instead. These funds tend to offer better returns than fixed deposits over similar time periods. And if you need monthly payouts — similar to the interest you’d receive from an FD — you can opt for a Monthly Income Plan (MIP). It gives you the best of both worlds: potentially better returns and regular income.

Key Factors to Consider Before Investing in Debt Mutual Funds

Debt funds might be safer than equity funds, but that doesn’t mean you should invest blindly. Here are a few things to evaluate first.

1. Expense Ratio

Just like with equity funds, the expense ratio matters for debt funds too. It includes all the fees you pay — management fees, operating costs, transaction fees, and any other charges.

Here’s why this is especially important for debt funds: since debt funds generally offer lower returns than equity funds, a high expense ratio can take a bigger bite out of your profits proportionally. Even a difference of 0.5% can make a noticeable impact on your net returns over time.

Always compare expense ratios before committing your money.

2. Management Fee

The management fee is the specific amount charged by the fund manager for managing your investment. It’s usually a fixed percentage of your invested amount and is charged on an annual basis.

A fund with a higher management fee will cost you more. But sometimes, paying a slightly higher fee is justified if the fund manager consistently delivers solid returns. The key is to assess whether the fee is worth the performance.

Look at the fund’s track record. If the manager has a history of generating good returns even after accounting for fees, it could still be a smart investment.

3. Your Risk Appetite

Even within debt funds, there are different levels of risk. A government securities fund is generally safer than a corporate bond fund, for example, because governments are less likely to default on their obligations.

Your risk appetite — how much risk you’re comfortable taking — should guide your choice of debt fund. If you’re extremely conservative, stick to funds that invest in high-quality, low-risk instruments. If you can handle a bit more risk for slightly better returns, you have more options to explore.

The point is, don’t just assume all debt funds are the same. Understand what’s inside the fund before you invest.

Equity Funds vs Debt Funds: A Clear Side-by-Side Comparison

Now that we’ve explored both types in detail, let’s put them side by side for a direct comparison. This should make the differences crystal clear.

What They Invest In

Equity Funds: Invest in shares of companies traded on the stock market. These funds are known to generate better returns than term deposits or debt-based funds.

Debt Funds: Invest in fixed-income securities like treasury bills, corporate bonds, commercial papers, government securities, and other money market instruments.

Risk Level

Equity Funds: Require a moderately high to high risk-taking appetite. The stock market is unpredictable, and short-term losses are common.

Debt Funds: Suitable for investors with a low to moderate risk-taking appetite. Returns are more stable and predictable.

Returns

Equity Funds: Offer comparatively higher returns in the long term. Historically, equity funds have outperformed most other investment options over extended periods.

Debt Funds: Offer lower returns compared to equity funds. However, they provide more consistency and predictability.

Taxation

Equity Funds: If you sell your equity fund units within 12 months of purchase, you pay a 15% tax on the capital gains (Short-Term Capital Gains tax).

Debt Funds: If you sell your debt fund units within 36 months of purchase, the gains are treated as Short-Term Capital Gains and taxed according to your income tax slab.

Investment Horizon

Equity Funds: Best suited for long-term financial goals — five years or more.

Debt Funds: Suitable for both short-term and long-term goals. Whether you’re parking money for a few months or investing for several years, there’s a debt fund that fits.

Tax-Saving Options

Equity Funds: You can claim tax deductions by investing up to ₹1,50,000 per year in ELSS (Equity Linked Savings Scheme) under Section 80C.

Debt Funds: No equivalent tax-saving option is available.

So, Which One Is Better — Equity or Debt?

This is the question everyone asks. And the honest answer is: neither one is universally “better.” They serve different purposes, and the right choice depends entirely on you.

Think of it this way:

- Equity funds are like planting a tree. It takes time. There might be storms along the way. But if you’re patient, it grows into something big and valuable.

- Debt funds are like a well-built shelter. They won’t grow as tall as the tree, but they’ll protect you from the rain and keep you safe when the weather gets rough.

The smartest investors don’t choose one over the other. They use both — equity for growth and debt for stability — creating a balanced portfolio that can weather different market conditions.

A Simple Framework for Choosing

Go with equity funds if:

- You have a long time horizon (5+ years)

- You can tolerate market volatility without losing sleep

- You want maximum growth potential

- You’re saving for distant goals like retirement or your child’s college education

Go with debt funds if:

- You want stability and predictability

- You have short to medium-term financial goals

- You prefer lower risk over higher returns

- You need a better alternative to savings accounts or fixed deposits

- You want regular income from your investments

Consider a mix of both if:

- You want balanced exposure to growth and safety

- You’re building a long-term portfolio but want some stability cushion

- You want to optimize your overall risk-return profile

Don’t Forget the Role of Age

Here’s a practical tip that many financial advisors swear by.

Your age should play a significant role in how you divide your investments between equity and debt.

The logic is simple:

- When you’re younger (20s and 30s), you have decades ahead of you. You can afford to take more risk because you have plenty of time to recover from any market downturns. So, a larger allocation to equity makes sense.

- As you get older (50s and beyond), your time horizon shrinks. You’re closer to needing the money — perhaps for retirement. You can’t afford big losses at this stage. So, gradually shifting more of your portfolio toward debt funds is a safer approach.

A popular rule of thumb is: 100 minus your age = the percentage you should invest in equity. So if you’re 30, put about 70% in equity and 30% in debt. If you’re 55, put about 45% in equity and 55% in debt.

It’s not a rigid rule, of course. Your personal situation, goals, and comfort with risk matter more than any formula. But it’s a useful starting point.

Final Thoughts

At the end of the day, both equity and debt mutual funds are useful instruments in an investor’s arsenal. They are not competitors but complementors.

The equity fund provides the growth, the excitement, and the long-term wealth creation. The debt fund provides the stability, the predictability, and the peace of mind.

The trick is to understand what each of these is bringing to the table, understand where you are in terms of risk profile and financial goals, and then create a portfolio that makes sense for you—not for your neighbor, not for the financial influencer on social media, but for you.

Before you invest in any fund, take a moment to honestly ask yourself:

- What am I investing for? (A specific goal or general wealth building?)

- How long can I keep my money invested? (Short-term or long-term?)

- How much risk am I truly comfortable with? (Be honest — not what you think you should say, but how you’d actually feel if your portfolio dropped 20%.)

- What’s my current financial situation? (Do I have an emergency fund? Am I carrying any debt?)

The answers to these questions will, of course, lead you to the right combination of equity and debt.

Investing is not about choosing the ‘best’ mutual fund. It is about choosing the ‘right’ mutual fund for your specific situation. And now that you know the difference between equity and debt mutual funds, you are in a far better position to do exactly that.

Start early, start now, and let time do the heavy lifting.

Learn More:

- How to Transfer Home Loan from One Bank to Another?

- How to Pay Electricity Bill through Credit Card

- How to Increase Credit Card Limit

- Home Loan Benefits for Women in India

- Best Banks for Gold Loan in India 2025

- Get SBI Yono Personal Loans? Helpful Tips to Get the Loan Fast

- 7-step checklist for fast ICICI Bank personal loan approval

- Airtel Payment Bank Loan: How to Get a ₹5,000 Loan in Just Minutes

Disclaimer: This blog is solely for educational purposes. The securities/investments quoted here are not recommendatory.