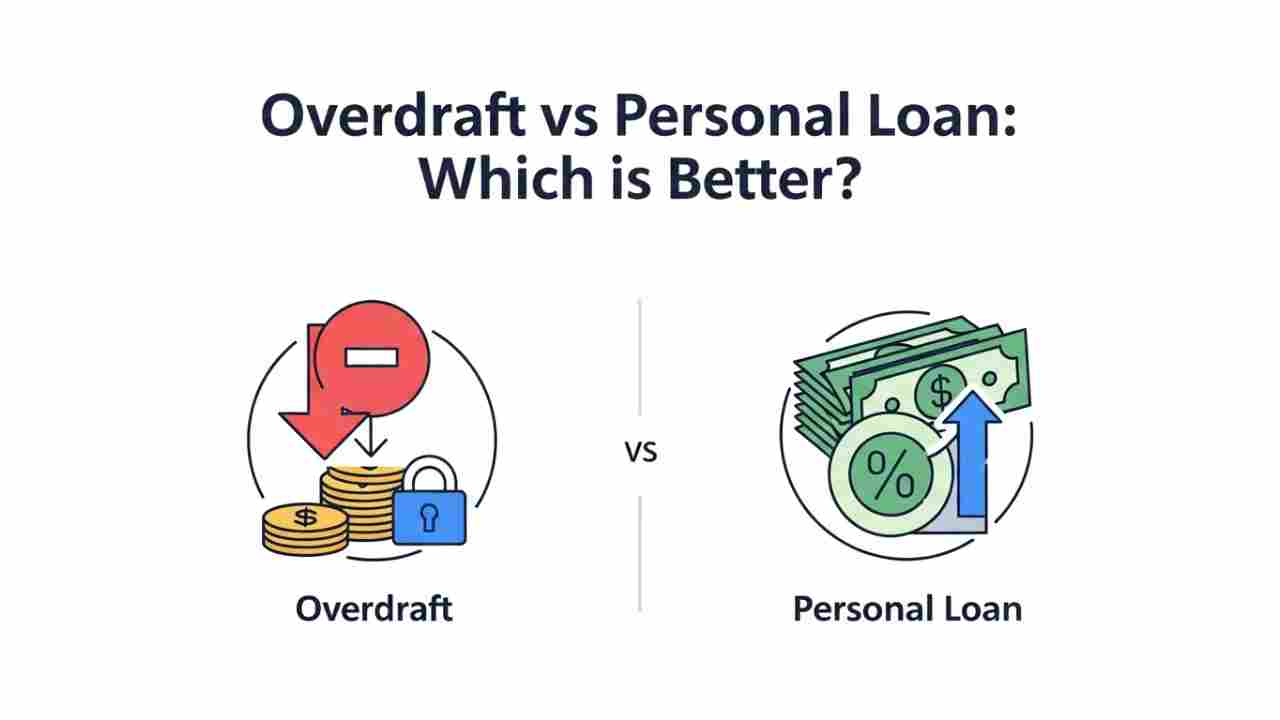

At times, we find ourselves needing a little more cash to cover our expenses—this could be for a business, a personal reason, or a matter involving a health emergency. In terms of borrowing, there are two most commonly used options: overdrafts and personal loans. These services allow you to gain money instantly but following different methodologies.

Within this blog, we will define overdraft facilities and personal loans, outline the differences between the two, and then help you determine which is the better option for you.

What is an Overdraft?

An overdraft facility is mainly extended to businessmen and professionals by banks. It is an arrangement in which the bank allows the customer to withdraw funds even if he or she does not have sufficient funds in the account up to the required amount.

Key Features of Overdrafts

- Flexible Withdrawal: You can withdraw money as and when needed, up to your overdraft limit.

- Interest on Used Amount: You pay interest only on the amount you actually withdraw, not on the entire limit.

- No Fixed Repayment: There’s no fixed repayment schedule. You can repay the amount at your own pace.

- Quick Access: Once approved, you can access funds instantly from your account.

- Best For: Fluctuating or uncertain fund requirements, short-term needs, or frequent small withdrawals.

What is a Personal Loan?

A personal loan is an unsecured loan offered by banks and financial institutions. You get a lump sum amount, which you repay in fixed monthly instalments over a set period.

Key Features of Personal Loans

- Lump Sum Disbursal: You get the entire approved amount at once.

- Fixed Repayment: You repay the loan in fixed monthly instalments over a stipulated period (usually 1-5 years).

- Interest on Entire Amount: You pay interest on the entire loan amount, not just what you use.

- Processing Time: It takes 2-3 working days for the loan to be approved and disbursed.

- Best For: Large, one-time expenses like medical bills, home renovation, or a big purchase.

Overdraft vs Personal Loan: Key Differences

Here’s a simple comparison to help you understand the differences:

| Parameter | Overdraft | Personal Loan |

|---|---|---|

| Loan Amount | Withdraw up to your limit as needed | Get a lump sum amount |

| Repayment | No fixed schedule. Repay at your own pace | Fixed monthly instalments |

| Interest Rate | Charged only on the amount withdrawn | Charged on the entire loan amount |

| Processing Time | Instant access once approved | 2-3 working days for disbursal |

| Fund Disbursal | Credit limit in your account. Withdraw as needed | Lump sum amount credited to your account |

Which is Better: Overdraft or Personal Loan?

The answer depends on your financial needs and repayment style.

Choose an Overdraft if:

- Your fund requirement is small and frequent.

- You need flexible repayment without a fixed schedule.

- You want quick access to funds for short-term needs.

- You prefer to pay interest only on the amount you use.

Choose a Personal Loan if:

- You need a lump sum amount for a big expense.

- You want a structured repayment plan with fixed monthly instalments.

- You prefer disciplined repayment to avoid overspending.

- Your requirement is for a medium to long tenure.

Real-Life Scenarios

Scenario 1: Small, Frequent Needs

If you run a small business and need occasional funds for expenses, an overdraft is better. You can withdraw as needed and repay when you have surplus cash.

Scenario 2: Big, One-Time Expense

If you need a large amount for a wedding, medical emergency, or home renovation, a personal loan is better. You get the entire amount at once and repay it in fixed instalments.

The Bottom Line

Both overdrafts and personal loans have their own pros and cons. An overdraft is the best financial option in the case of flexible and short-term requirements, while a personal loan would work efficiently in one-time expenses.

Be informed about your finance situation, demands, and repayment ability before selecting whether or not to go for an overdraft or a personal loan.

Learn More:

- How to Start Investing in Mutual Funds in India – Step-by-Step Process for Beginners

- Difference Between Mutual Funds and Stocks – Which is Better for Beginners?

- Understanding NAV (Net Asset Value) in Mutual Funds – What It Means and Why It Matters

- Risks Involved in Mutual Fund Investments – Common Risks and How to Manage Them

Disclaimer: The information provided here is for general educational purposes and should not be taken as investment counsel. Investment in stocks is risky and the prices may fluctuate either way. Do your own research or consult a financial advisor prior to investing your capital.