Mutual fund investment is now one of the most trending methods of generating wealth in India. But investors are confused regarding the tax law when they liquidate their mutual fund units. Mutual fund taxation is important because it will directly impact your net return. Due to recent changes made in tax law, especially in Budget 2023 and additional updates in 2024-25, it is necessary to keep yourself updated regarding the new rules.

This guide will make you aware of all about mutual fund taxation in the simplest form, such as capital gains tax, indexation relief, and calculating your own tax liability.

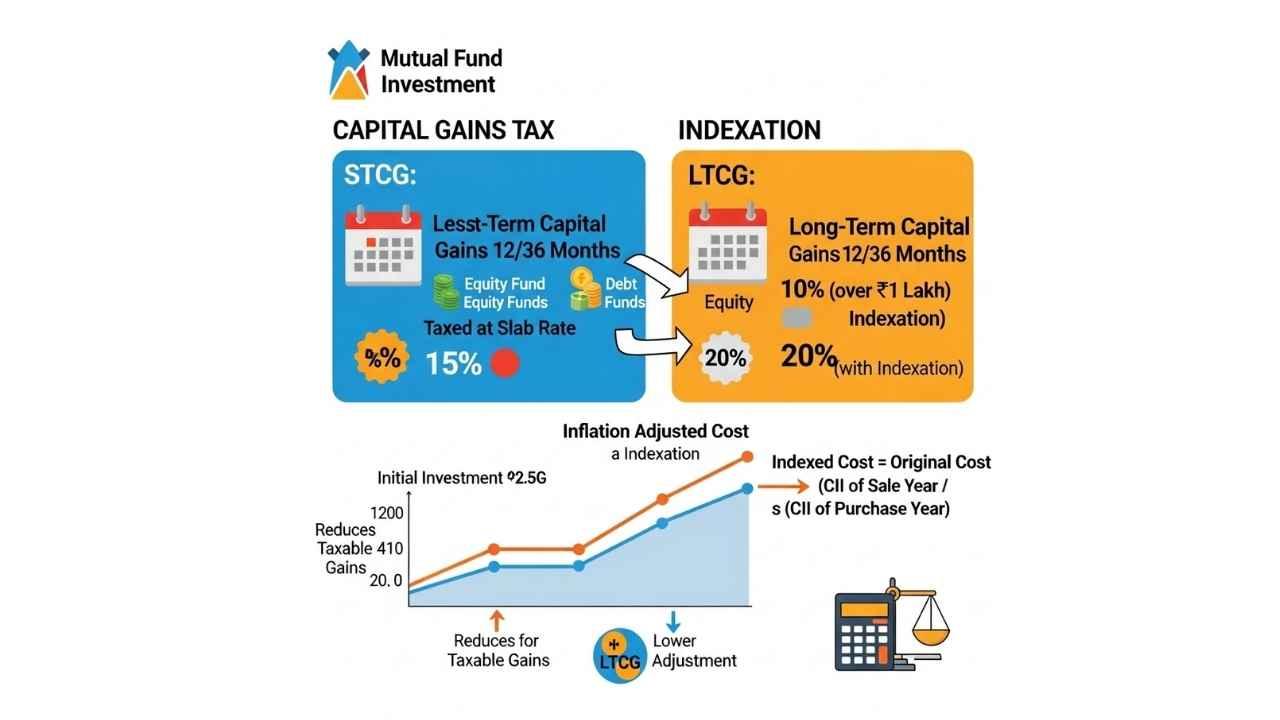

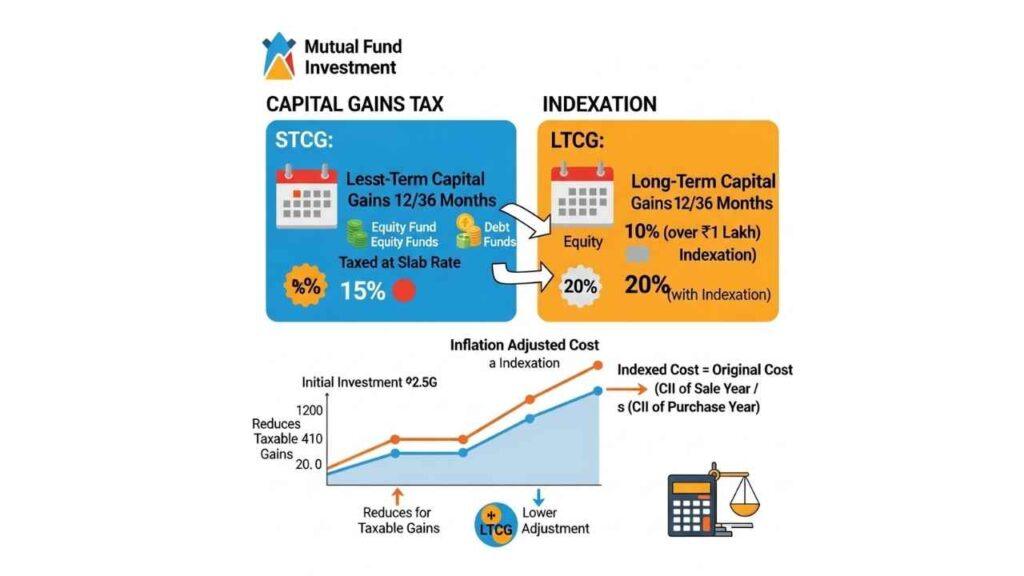

What is Mutual Fund Capital Gains Tax?

Capital gains tax is the tax you owe on the profit you gain when selling your mutual fund units. When you cash in your mutual fund investments for an amount greater than you invested, the excess is referred to as capital gains, and this gain is taxed.

For instance, if you purchased mutual fund units of ₹1,00,000 and sold them at ₹1,50,000, your capital gain is ₹50,000. This ₹50,000 will be taxed in line with certain rules depending on the kind of fund and the duration of holding.

Types of Capital Gains

Capital gains from mutual funds are classified into two categories based on how long you hold your investments:

Short-Term Capital Gains (STCG)

These are profits from selling mutual fund units within a short period. The holding period varies by fund type:

- Equity funds: Less than 12 months

- Debt funds: Less than 36 months (for funds purchased before April 1, 2023)

- Hybrid funds: Depends on equity allocation

Long-Term Capital Gains (LTCG)

These are profits from selling units after holding them for a longer period:

- Equity funds: 12 months or more

- Debt funds: 36 months or more (for funds purchased before April 1, 2023)

Current Tax Rules for Different Types of Mutual Funds

The tax rules vary significantly based on the type of mutual fund you invest in. Here’s a detailed breakdown:

Equity Mutual Funds Taxation

Equity funds are those that invest at least 65% of their assets in Indian stocks. The latest tax rules effective from July 23, 2024, are:

Short-Term Capital Gains (Less than 12 months)

- Tax rate: 20% plus cess

- Previously, it was 15%

Long-Term Capital Gains (12 months or more)

- Tax rate: 12.5% on gains above ₹1.25 lakh

- Exemption: First ₹1.25 lakh of LTCG is tax-free in a financial year

- Previously, it was 10% on gains above ₹1 lakh

Debt Mutual Funds Taxation

Debt fund taxation has undergone significant changes since Budget 2023. The rules depend on when you purchased the units:

For Units Purchased Before April 1, 2023:

- Holding period less than 2 years: Taxed at your income tax slab rate

- Holding period more than 2 years: 12.5% tax without indexation benefit

For Units Purchased On or After April 1, 2023:

- All gains are taxed at your income tax slab rate, regardless of holding period

- No indexation benefit available

Hybrid Mutual Funds Taxation

The taxation of hybrid funds depends on their equity allocation:

Equity-oriented hybrid funds (65% or more in equity):

- Follow the same tax rules as equity funds

Debt-oriented hybrid funds (less than 65% in equity):

- Follow the same tax rules as debt funds

International and Gold Mutual Funds

From April 1, 2025, these funds will have new tax rules:

For investments made on or after April 1, 2025:

- LTCG: 12.5% if held for more than 2 years

- STCG: Taxed at income tax slab rates

Understanding Indexation in Mutual Funds

Indexation is a method to adjust the purchase price of your investment for inflation. This helps reduce your taxable capital gains by accounting for the decrease in money’s purchasing power over time due to inflation.

How Indexation Works

The government publishes a Cost Inflation Index (CII) every year. For FY 2024-25, the CII is 363. For FY 2025-26, the CII is 376.

The indexation formula is:

Indexed Cost = (CII of sale year ÷ CII of purchase year) × Original purchase price

Indexation Example

Let’s say you bought debt mutual fund units for ₹1,00,000 in FY 2016-17 (CII = 264) and sold them in FY 2020-21 (CII = 301):

- Indexed Cost = (301 ÷ 264) × ₹1,00,000 = ₹1,13,999

- If you sold for ₹1,50,000, taxable gain = ₹1,50,000 – ₹1,13,999 = ₹36,001

- Tax payable = 20% of ₹36,001 = ₹7,200 (approximately)

Without indexation, you would pay tax on ₹50,000, resulting in ₹10,000 tax.

Important Note About Indexation

Indexation benefit is no longer available for most mutual fund investments:

- Not available for debt funds purchased after April 1, 2023

- Not available for equity funds (never was available)

- Limited availability for debt funds purchased before April 1, 2023

Dividend Taxation in Mutual Funds

Since April 1, 2020, all dividend income from mutual funds is taxable in your hands. Previously, mutual funds paid Dividend Distribution Tax (DDT), but this has been abolished.

How Dividend Taxation Works

- Dividends are added to your total income and taxed at your applicable income tax slab rate

- TDS (Tax Deducted at Source) of 10% is applicable if annual dividends exceed ₹10,000 from a single mutual fund

- You can claim this TDS when filing your income tax return

Example of Dividend Taxation

If you earn ₹15,000 as dividends from mutual funds:

- TDS deducted: ₹1,500 (10% on amount above ₹10,000)

- Amount received: ₹13,500

- Tax liability: Based on your income tax slab rate

Special Rules for SIP Investments

Each SIP installment is treated as a separate purchase with its own purchase date and holding period. This means:

FIFO Method Application

When you redeem SIP units, the First In, First Out (FIFO) method applies:

- Units purchased first are considered sold first

- Each installment’s holding period is calculated separately

- Tax treatment depends on individual holding periods

SIP Tax Calculation Example

Suppose you started a monthly SIP of ₹10,000 in an equity fund:

- January 2023: Purchased units at NAV ₹50 (200 units)

- February 2023: Purchased units at NAV ₹55 (182 units)

- March 2023: Purchased units at NAV ₹60 (167 units)

If you redeem 300 units in February 2024 at NAV ₹70:

- January units (200): Held for >12 months = LTCG

- February units (100): Held for exactly 12 months = LTCG

- Tax: 12.5% on gains above ₹1.25 lakh exemption

Also Read: How to Start Investing in Mutual Funds in India – Step-by-Step Process for Beginners

How to Calculate Your Mutual Fund Tax

Step-by-Step Calculation Process

Step 1: Determine the Fund Type

- Equity fund (≥65% equity)

- Debt fund (<65% equity)

- Hybrid fund (check equity allocation)

Step 2: Calculate Holding Period

- Count from purchase date to sale date

- Use FIFO for SIP investments

Step 3: Identify Capital Gains Type

- Short-term or long-term based on holding period

Step 4: Apply Appropriate Tax Rate

- Use current tax rates based on fund type and holding period

Step 5: Consider Exemptions

- ₹1.25 lakh LTCG exemption for equity funds

- Income tax slab rates for debt funds

Practical Tax Calculation Example

Equity Fund Investment:

- Purchase: ₹2,00,000 (held for 18 months)

- Sale: ₹3,00,000

- Capital Gain: ₹1,00,000

- Tax: Nil (within ₹1.25 lakh exemption)

Debt Fund Investment (purchased before April 1, 2023):

- Purchase: ₹1,00,000 (held for 3 years)

- Sale: ₹1,40,000

- Capital Gain: ₹40,000

- Tax: 12.5% of ₹40,000 = ₹5,000

Tax-Saving Tips for Mutual Fund Investors

1. Hold Investments for Long Term

Long-term investments generally attract lower tax rates. For equity funds, holding for more than 12 months can save significant taxes.

2. Use Tax Loss Harvesting

Offset capital gains with capital losses from other investments to reduce your overall tax liability.

3. Plan Your Redemptions

Time your redemptions strategically:

- Spread large redemptions across financial years

- Stay within the ₹1.25 lakh LTCG exemption limit for equity funds

4. Choose Growth Over Dividend Options

Growth options are more tax-efficient as you control when to realize gains, while dividends are taxed immediately.

5. Consider Asset Allocation

Balance your portfolio between equity and debt funds based on your tax bracket and investment horizon.

Common Mistakes to Avoid

1. Ignoring the Purchase Date

Each SIP installment has a different purchase date. Don’t assume all units have the same holding period.

2. Not Tracking Cost Inflation Index

For eligible debt fund investments, always use the latest CII for accurate tax calculation.

3. Forgetting About TDS

TDS on dividends can affect your cash flow. Plan accordingly and claim it during ITR filing.

4. Not Maintaining Proper Records

Keep detailed records of all purchases, sales, and dividend payments for accurate tax filing.

5. Panic Selling Before Completing Holding Period

Selling just before completing the long-term holding period can result in higher tax rates.

Filing Taxes on Mutual Fund Gains

Required Documents

- Account statements from mutual fund companies

- Capital gains statements (provided by fund houses)

- TDS certificates for dividends

- Cost Inflation Index tables (for applicable investments)

ITR Forms to Use

- ITR-2: For individuals with capital gains

- ITR-3: For business income along with capital gains

Important Deadlines

- ITR filing deadline: July 31 (may be extended)

- Advance tax payments: Quarterly (if applicable)

Impact of Recent Tax Changes

Budget 2023 Changes

Major impact on debt fund taxation:

- Removed indexation benefit for new debt fund investments

- Made all debt fund gains taxable at slab rates (for post-April 2023 purchases)

Budget 2024 Changes

Revised rates for equity funds:

- Increased STCG rate from 15% to 20%

- Increased LTCG rate from 10% to 12.5%

- Raised exemption limit from ₹1 lakh to ₹1.25 lakh

Future Outlook

Expect continued changes in mutual fund taxation as the government balances revenue needs with investment promotion.

Conclusion

Mutual fund taxation is something that you must know to make intelligent investment decisions. The main points are:

- Equity funds offer better tax treatment for long-term investors with the ₹1.25 lakh exemption

- Debt funds purchased after April 1, 2023, have lost most tax advantages

- Indexation benefits are now limited to specific debt fund investments made before April 1, 2023

- SIP investments require careful tracking of individual purchase dates

- Dividend income is now taxable at your slab rate

Invest in mutual funds after considering returns and tax implications. Get professional advice from a qualified tax consultant depending on your individual financial situation and investment objectives.

Tax regulations keep changing, so keep yourself informed about the current rules and modify your investment plan accordingly. The intent is to achieve maximum after-tax returns and create wealth in the long run through disciplined mutual fund investing.

Learn More:

- How to Start Investing in Mutual Funds in India – Step-by-Step Process for Beginners

- Difference Between Mutual Funds and Stocks – Which is Better for Beginners?

- Understanding NAV (Net Asset Value) in Mutual Funds – What It Means and Why It Matters

- Risks Involved in Mutual Fund Investments – Common Risks and How to Manage Them