When investing in mutual funds, everyone is familiar with SIP (Systematic Investment Plan) and SWP (Systematic Withdrawal Plan). There is one strong alternative that usually goes unnoticed—STP (Systematic Transfer Plan).

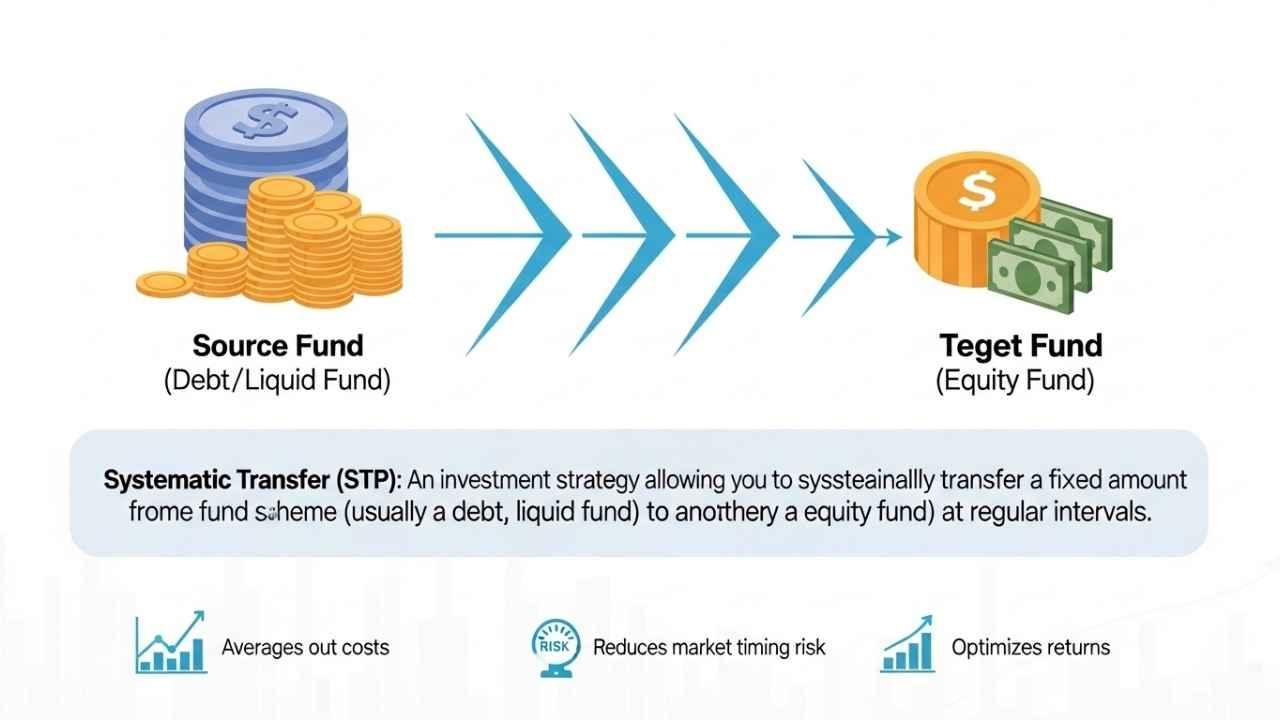

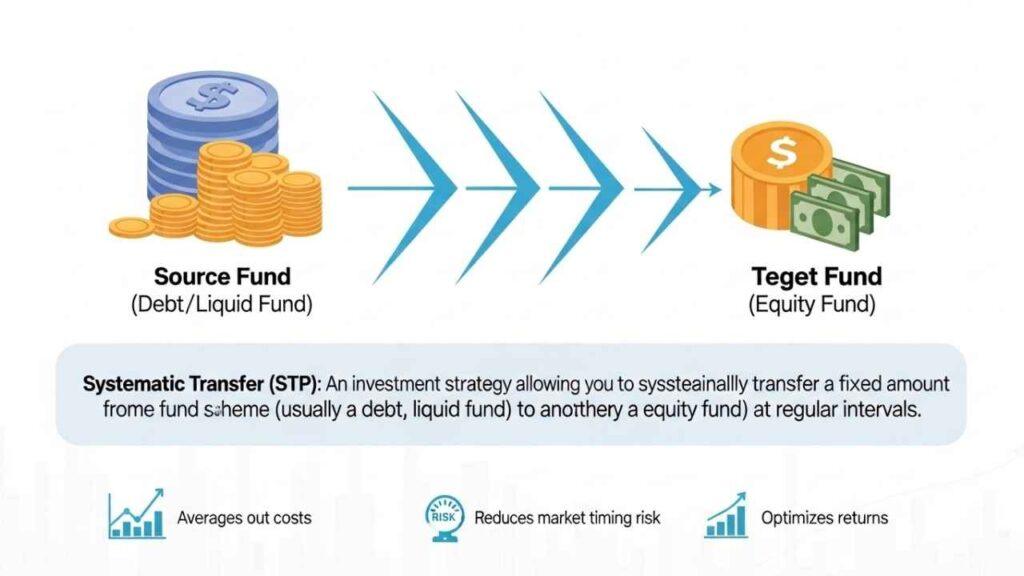

In plain language, an STP lets you move money in a systematic manner from one mutual fund to another. This is normally carried out from a debt fund to an equity fund or vice versa, as per your financial objective and market scenario.

Consider STP as a corridor between two funds. Rather than transferring an amount in bulk at one time, you can send small amounts of money periodically, cutting down on risks and diversifying your portfolio.

What is STP in Mutual Funds?

A Systematic Transfer Plan (STP) is a facility that lets investors transfer a fixed amount of money at regular intervals from one mutual fund scheme to another.

- The fund you transfer money from is usually a debt fund (stable and safe).

- The fund you transfer money to is usually an equity fund (growth-oriented but risky).

This way, your money doesn’t just sit idle—it earns returns in the debt fund while gradually moving into equities.

How Does STP Work?

Here’s how an STP works step by step:

- Invest in a Source Fund – You put a lump sum amount in a mutual fund (commonly a liquid or debt fund).

- Set Transfer Amount & Frequency – Decide how much money should be transferred and how often (daily, weekly, monthly, etc.).

- Automatic Transfer – On each scheduled date, the chosen amount moves from the source fund to the target fund.

- Portfolio Growth – Your money earns steady returns in the source fund while gradually entering the target fund for long-term growth.

Example: You invest ₹5 lakh in a liquid fund and start an STP of ₹20,000 per month into an equity fund. Over time, you reduce the risk of investing all ₹5 lakh in the stock market at once while still allowing your money to grow.

Key Benefits of STP

- Reduces Market Timing Risk – Instead of investing a lump sum in equities at once, you spread your investment.

- Dual Benefit – Money stays invested in a debt fund (earning returns) before moving to equity.

- Rupee Cost Averaging – Similar to SIP, you buy more units when the market is low and fewer when it’s high.

- Flexibility – You can choose the amount, frequency, and duration of transfers.

- Ideal for Lump Sum Investors – Especially useful for those who receive bonuses, retirement funds, or large savings.

Types of STP

Mutual funds offer different types of STPs based on how the transfer is structured:

- Fixed STP – A fixed sum is transferred from the source fund to the target fund.

- Capital Appreciation STP – Only the profits (returns) earned in the source fund are transferred.

- Flexi STP – The transfer amount can change depending on market conditions or investor choice.

Who Should Invest Through STP?

STP is suitable for:

- Lump Sum Investors – Those with large amounts to invest but want to avoid market timing risk.

- Conservative Investors – People who want to park money in debt funds first before entering equities.

- Retirees – Who prefer transferring from equity to debt for safety.

- Goal-Based Investors – Those who want to balance risk and growth while planning for long-term goals.

Taxation in STP

Each transfer in STP is considered a redemption from the source fund and a purchase in the target fund. This means taxation rules apply:

- Debt Fund Transfers – Gains are taxed as per your income tax slab.

- Equity Fund Transfers – Short-term gains (less than 1 year) are taxed at 15%, and long-term gains (above ₹1 lakh per year) are taxed at 10%.

So, while STP is useful, you must keep taxation in mind when planning.

Real-Life Example of STP

Imagine Ramesh gets a bonus of ₹6 lakh. Instead of investing the whole amount into equity funds at once (which can be risky if the market is high), he parks it in a liquid fund. Then, he sets up an STP of ₹50,000 per month into an equity fund.

This way:

- His money earns interest in the liquid fund.

- He benefits from rupee cost averaging in equities.

- He avoids the stress of timing the market.

Conclusion

A Systematic Transfer Plan (STP) is an intelligent investment plan for people who wish to transfer funds from one mutual fund to another systematically. It gives the advantage of safety, increase in value, and lower risk. Whether you are a retired person, a salaried person receiving a bonus, or one planning long-term investments, STP will guide you to invest your money wisely.

Rather than keeping your money idle or gambling with it all at one go, let STP do its job—slow, steady, and strategic.

Learn More:

- How to Start Investing in Mutual Funds in India – Step-by-Step Process for Beginners

- Difference Between Mutual Funds and Stocks – Which is Better for Beginners?

- Understanding NAV (Net Asset Value) in Mutual Funds – What It Means and Why It Matters

- Risks Involved in Mutual Fund Investments – Common Risks and How to Manage Them

FAQs

1. What is the minimum amount required for STP?

Usually ₹500–₹1,000 per transfer, depending on the fund.

2. Can I stop an STP anytime?

Yes, STPs are flexible—you can stop or modify them whenever needed.

3. Is STP better than SIP?

SIP is best for regular small savings, while STP is better for lump sum investments.

4. Does STP guarantee returns?

No, returns depend on the performance of the funds chosen.

5. Can I do STP from equity to debt funds?

Yes, you can transfer from equity to debt if you want safety as you near your financial goals.