Investing is not only about increasing wealth—it’s also about wisely using that wealth. Most investors take into consideration how to invest money via SIPs (Systematic Investment Plans), but few bother to think about how to withdraw their money intelligently. That’s where SWP (Systematic Withdrawal Plan) helps.

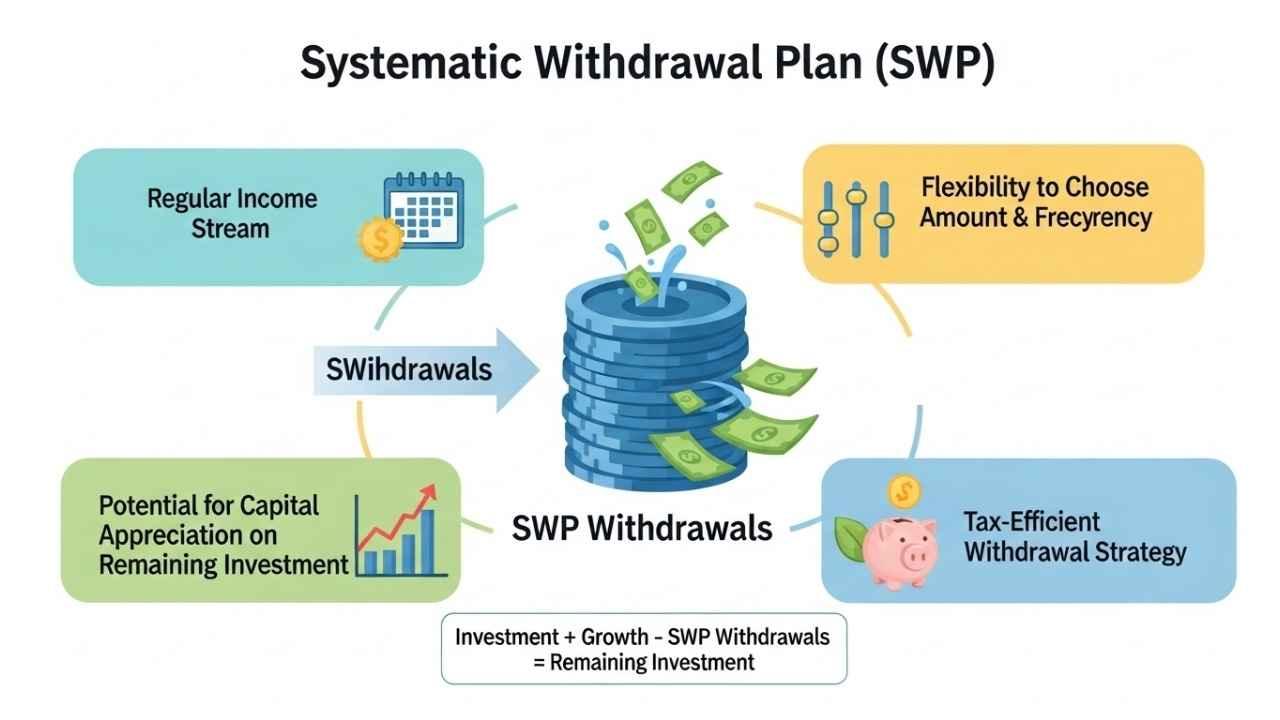

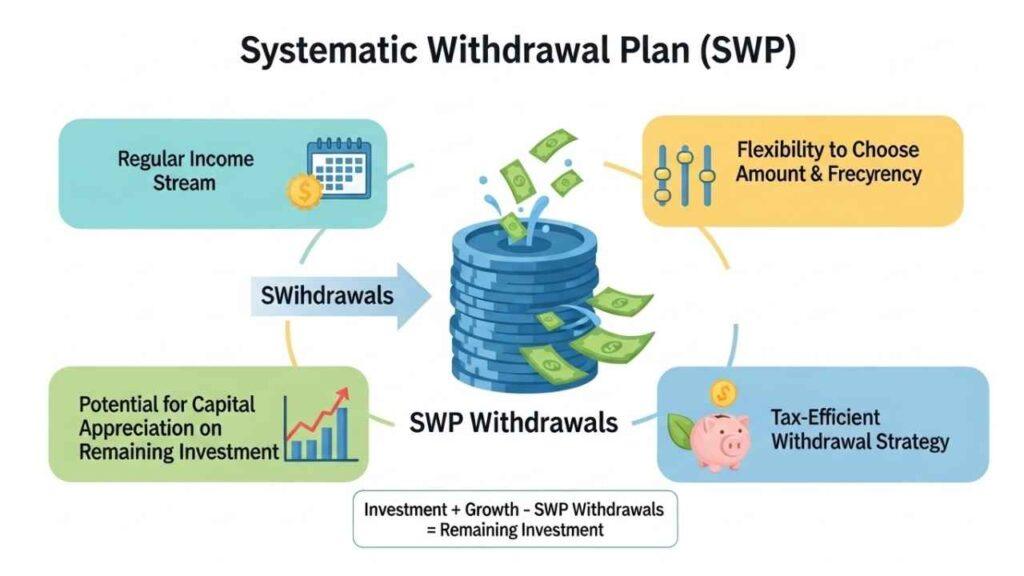

Consider SIP as a method for creating wealth and SWP as a method for living off that wealth. You can systematically withdraw a fixed amount of money from your mutual fund investment at regular time intervals through SWP so that you get regular income and your remaining investment keeps growing.

This works particularly well for retirees, individuals looking for a steady second income, or anyone looking for systematic withdrawals rather than withdrawing the entire corpus at one time.

What is SWP?

A Systematic Withdrawal Plan (SWP) is an amenity provided by mutual funds where you can withdraw a specific amount of money at fixed intervals—monthly, quarterly, or annually—from your invested corpus.

Rather than redeeming all your units of the mutual fund at one time, SWP allows you to redeem them in installments. Every time you draw, a portion of the units are redeemed at the prevailing Net Asset Value (NAV).

For instance, if you have invested ₹10 lakh in a mutual fund and initiated an SWP of ₹20,000 a month, the fund will itself redeem sufficient units every month to pay you that amount, and the balance of your investment remains invested.

This provides you with liquidity (sustainable cash flow) and growth (unutilized money continues to earn returns).

How Does SWP Work?

The working of an SWP is simple and systematic:

- Invest in a Mutual Fund – First, you put a lump sum amount in a mutual fund scheme.

- Set Withdrawal Amount & Frequency – You choose how much you want to withdraw and how often (monthly, quarterly, etc.).

- Automatic Redemption – On the chosen date, the fund redeems enough units to give you the requested amount.

- Balance Continues to Grow – The remaining money stays invested and keeps earning returns.

Example: Suppose you invest ₹10,00,000 in a mutual fund with an average return of 10% per year. If you start an SWP of ₹25,000 per month, the withdrawals will give you regular income, and the balance amount can still grow over time depending on market performance.

Benefits of SWP

SWP offers several advantages:

- Regular Income – Perfect for retirees or those looking for monthly cash flow.

- Market Volatility Protection – Since withdrawals are spread out, you don’t depend on market timing.

- Wealth Preservation – Unlike withdrawing the whole amount, SWP ensures part of your money continues to grow.

- Tax Efficiency – Only the withdrawn portion is taxed, not the entire investment.

- Discipline in Withdrawals – Prevents overspending or panic selling.

SWP can be compared to a “salary” from your own investments—steady, reliable, and flexible.

Types of SWP in Mutual Funds

There are different types of SWP to suit different needs:

- Fixed SWP – Withdraw a fixed amount at regular intervals.

- Appreciation SWP – Withdraw only the profits/returns earned, leaving the capital untouched.

- Customized SWP – Allows flexibility in choosing amount and frequency as per your needs.

How to Start an SWP

Starting an SWP is simple and requires just a few steps:

- Invest a lump sum amount in a mutual fund.

- Fill out the SWP form with withdrawal amount, frequency, and duration.

- Submit the form online or to the mutual fund company.

- Withdrawals start on the chosen date.

Most mutual fund platforms allow you to set up SWPs online within minutes.

Taxation in SWP

- Withdrawals in SWP are considered redemptions and taxed as per capital gains tax rules.

- Equity Funds:

- Short-term (less than 1 year) → 15% tax

- Long-term (more than 1 year) → 10% tax (gains above ₹1 lakh)

- Debt Funds (after 2023 changes): Gains are taxed as per your income tax slab.

This makes SWP more tax-efficient compared to traditional options like fixed deposits.

Common Mistakes to Avoid in SWP

- Choosing a very high withdrawal amount (may deplete corpus fast).

- Not reviewing fund performance regularly.

- Using equity funds for short-term SWPs (can be risky).

- Ignoring taxation impact.

SWP vs. Traditional Fixed Deposits

| Feature | SWP | Fixed Deposit (FD) |

|---|---|---|

| Returns | Market-linked (higher potential) | Fixed, lower |

| Taxation | Capital gains tax (more efficient) | Interest fully taxable |

| Flexibility | High (can modify or stop anytime) | Low (fixed tenure, penalties) |

| Inflation Protection | Better (growth potential) | Poor |

Clearly, SWP offers better flexibility and tax efficiency compared to FDs.

Conclusion

A Systematic Withdrawal Plan (SWP) in mutual funds is a prudent and disciplined method of earning regular income while continuing to invest your money. It offers flexibility, tax advantages, and wealth retention—making it an ideal choice for retirees, those looking for passive income, or anyone wishing to achieve financial security.

Instead of withdrawing everything at once, SWP allows you to enjoy the fruits of your investments gradually, like receiving a salary from your own wealth.

Learn More:

- How to Start Investing in Mutual Funds in India – Step-by-Step Process for Beginners

- Difference Between Mutual Funds and Stocks – Which is Better for Beginners?

- Understanding NAV (Net Asset Value) in Mutual Funds – What It Means and Why It Matters

- Risks Involved in Mutual Fund Investments – Common Risks and How to Manage Them

FAQs

1. What is the minimum amount for SWP?

Usually ₹500–₹1,000 per month, depending on the fund house.

2. Can I stop my SWP anytime?

Yes, SWP is flexible—you can modify, pause, or stop it anytime.

3. Is SWP risk-free?

No, returns depend on the mutual fund’s performance, but spreading withdrawals reduces risk.

4. Who should choose SWP?

Retirees, people needing regular income, or anyone with lump sum investments.

5. Is SWP better than FD for retirees?

Yes, SWP can provide better returns, flexibility, and tax efficiency compared to fixed deposits.